Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present. - John Kenneth Galbraith

Much ink has been spilled on what happened with Silicon Valley Bank and why it failed. Having only witnessed GFC in 2008 from the sidelines as a freshman in college, seeing the crisis unfold now from within the industry and the reverberations felt given the second biggest bank failure in U.S on March 10th was interesting to say the least.

I initially thought of writing up something on Silicon Valley Bank and its business, and the response by fintechs in terms of product launches but the more I read, the more threads I found myself pulling on. 15k words later and a few weekends since the crisis, I found myself having woven together and chronicled the history on what really happened by trying to answer the following -

The SVB crisis over the past month bought back memories of all the discussions during/post GFC of things that had happened during the Great Depression/Savings and Loan crisis in the 80s yet it feels like with every passing generation, we forget the lessons of the past crisis. History is largely a chronicle of mistakes to be avoided and hence, I have always found myself resonating with a quote attributed to Cicero - “History is the witness that testifies to the passing of time; it illumines reality, vitalizes memory, provides guidance in daily life and brings us tidings of antiquity.”

Let’s jump in and hope you enjoy the post!

Table of Contents

Bank runs and creation of FDIC

What does a bank really do?

Understanding SVB and its business model

View on U.S economy/fundraising post GFC(Great Financial Crisis)

What transpired over the past year and on the fateful week of March 6th?

How did Fintechs and other industry players respond?

What does the future hold?

Bank runs and creation of FDIC

On March 12th, 1933, Americans all across the country found themselves listening in on the first of many fireside chats by Franklin Delano Roosevelt. The focus for this chat was to talk about banks and what plans had been drawn up by the administration post inauguration(just a week before). Here was a key section on how banks(albeit a very 19th century and incorrect view that a lot of people still hold which is that banks need deposits for lending. SVB crisis brought forth this view again from a lot of VCs as well) and banking works from FDR

First of all let me state the simple fact that when you deposit money in a bank the bank does not put the money into a safe deposit vault. It invests your money in many different forms of credit-bonds, commercial paper, mortgages and many other kinds of loans. In other words, the bank puts your money to work to keep the wheels of industry and of agriculture turning around. A comparatively small part of the money you put into the bank is kept in currency -- an amount which in normal times is wholly sufficient to cover the cash needs of the average citizen. In other words the total amount of all the currency in the country is only a small fraction of the total deposits in all of the banks.

What, then, happened during the last few days of February and the first few days of March? Because of undermined confidence on the part of the public, there was a general rush by a large portion of our population to turn bank deposits into currency or gold. -- A rush so great that the soundest banks could not get enough currency to meet the demand. The reason for this was that on the spur of the moment it was, of course, impossible to sell perfectly sound assets of a bank and convert them into cash except at panic prices far below their real value.

What necessitated this fireside chat? Since the onset of the Great Depression, bank runs became a common thing and led to failure of thousands of banks. To be specific, 650 banks failed in 1929, more than 1,300 in 1930; and over 9,000 banks would fail in total. In the first few months of 1933, there was another wave of bank runs that culminated in FDR declaring a bank holiday, gradual opening of the banks, signing of the Emergency bank act, and finally on June 16th, 1933, the signing of the Banking Act also commonly known as the Glass-Steagall Act. It was in the Banking Act of 1933 where we see the creation of FDIC(Federal Deposit Insurance Corporation).

Before we look at what is FDIC, how it works, what is it tasked to do, here is a fantastic clip of George Eccles talking about bank run on First Security Corporation during the Great Depression.

There are several things at play here in the video. The most important being human psychology. Homo Economicus or Rational choice theory in essence highlights that at the centre of the decisions being made lies a person bounded by rationality and complete information. Now, I am not sure how many economists or people continue to believe in this but if you were to just naturally observe ones own or other people and their behaviours in times of distress, things become fairly clear in how irrational we can be in situations. Bank runs in its essence is “damned if you do and damned if you don’t” kind of situation. Later into the post, we will look into how this played out with SVB and the depositors. Even though, Franklin Roosevelts statement “we have nothing to fear but fear itself.” was meant for the broader economic malaise, it is this belief and squashing bank runs, that lies in the origin of FDIC

The Banking Act of 1933 led to the establishment of the Federal Deposit Insurance Corporation in 1933 with the following 3 mandates at the core of its operations

Source - FDIC

Just a slight digression here. The U.S. was the first country to introduce a national deposit insurance system but over the ensuing decades, the system has taken prevalence and the following countries all offer insurance in some form of the other

Most people and anyone not involved in the financial services industry are usually only familiar with what is FDIC insurance . The birth of FDIC in 1933 also saw an initial ceiling on insured deposits of up to $2500 per account which since then has increased to $250,000(last increase was from $100k to $250k in 2008)

Source - American Deposit Management

What does this insurance on your bank account actually mean? Think of it as no different from an insurance policy that promises to pay out a certain amount in the case of a condition being met for which the policy is taken out. In this case, FDIC promises account holders that in if the bank where they held their account was to fail, they will be paid back with 100% certainty the full $250k that is protected by law. How has reality actually panned out? Fairly good when it comes to insured deposits. No customer of a bank that is FDIC insured has ever lost a single dollar.

How has FDIC over all these decades gone about ensuring the safety of these deposits and that the trust in the system remains unbridled? There are 3 core things that underpin FDIC operations

The Deposit Insurance Fund(DIF), and how it is underpins the whole deposit insurance program

The DIF gains funds through what is called a bank assessment. This is in essence a fee that the FDIC charges banks(Credit Unions are not covered by this. More on this later). This fee is calculated every quarter by taking the assessment base(average consolidated total assets minus average tangible equity) and an assessment rate based on factors such as

Small(generally, those with less than $10 billion in assets) vs large banks

Formula using financial data and CAMELS (capital adequacy, asset quality, management, earnings, liquidity, and sensitivity) ratings.

Risk Categories I through IV, with I being the lowest risk

From FDIC report - The assessment base has always been more than just insured deposits. From 1935 to 2010, a bank's assessment base was about equal to its total domestic deposits. As required by the Dodd- Frank Act, however, the FDIC amended its regulations effective April 2011 to define a bank's assessment base as its average consolidated total assets minus its average tangible equity.

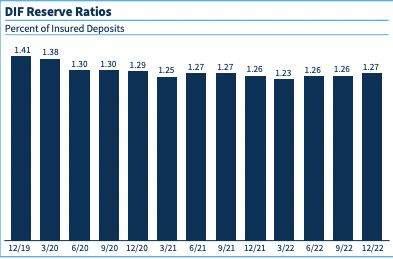

We might be in the infancy of a potential banking crisis(yet to see what the end result on DIF might be) given the rate hikes and impact on solvency but the 2008 and 2013 time period can serve as a gentle reminder on how chaotic things were and the seriousness of the banking crisis during GFC.

There were 489 bank failures in that time period and even though the economy had started recovering in 2009, that was when the expenses far surpassed the revenues for FDIC and over the ensuing quarters, the DIF(according to the accounting numbers) actually went negative

Source - FDIC

Here is an excerpt from one of the FDIC reports detailing how things played out during the GFC

The FDIC could have borrowed from the Treasury, which it had done in the early 1990s during the bank and thrift crisis, but it chose not to borrow. Borrowing would not have helped maintain a positive fund balance, or net worth, whereas a special assessment would. Despite higher assessment rates and the special assessment, mounting losses from actual failures as well as reserves set aside for anticipated failures caused the fund balance to fall below zero in the second half of 2009 and hit a low point of negative $20.9 billion by the end of the year. With the rise in actual and projected failures, by September 2009 the DIF’s liquidity needs threatened to exceed its liquid assets as early as 2010. If this potential squeeze on the liquid assets of the DIF were not addressed, it threatened to compromise the FDIC’s ability to pay depositors promptly. To address this issue, the FDIC adopted a novel approach that required the banking industry to prepay its quarterly risk-based assessments for the fourth quarter of 2009 and for the next three years. In contrast to a special assessment, a prepaid assessment did not impair bank earnings and capital under applicable accounting rules. The prepayment was counted on the banks’ balance sheets as an asset that was reduced each quarter as each prepaid assessment came due. Because banks were holding significant amounts of cash at the time, the FDIC believed that most of the prepayments would be drawn from banks’ available cash and excess reserves at the Federal Reserve without significantly affecting banks’ lending activities. This approach not only generated sufficient liquidity for the DIF to weather the crisis, but it also earned widespread banking industry support. Again, the FDIC had decided not to use its authority to borrow from the Treasury to meet liquidity needs. Prepaid assessments ensured that the DIF remained directly industry funded; and prepayments, unlike Treasury borrowing, accrued no interest.

The reason for highlighting this excerpt is the constant clarion call from people to do whatever it takes to save the banks even if it means taking taxpayer money without realising that the optics/second order effects of such things should be considered. FDIC has been a well run organisation and is funded via the banks that utilise the deposit insurance. As of Q4,22, the Deposit Insurance Fund (DIF) balance increased by $2.8 billion to $128.2 billion and so far the SVB hit on that balance has been ~$20B. There are still ways to go before we get closer to worst case scenario around banking crisis and losses on DIF.

Source - FDIC

When a bank does go under and falls under the receivership of the FDIC, there are 2 primary options/lens with which the FDIC looks at the situation

Purchase and Assumption Transaction. FDIC predominantly works towards asserting its power and preference towards another bank acquiring the bank that has been put under receivership. Insured depositors of the failed bank immediately become depositors of the assuming bank and have access to their insured funds. There is also an optionality for the acquiring bank to purchase loans and other assets of the failed bank.

Deposit Payoff. When there is no open bank acquirer for the deposits, the FDIC will pay the depositor directly by check up to the insured balance in each account. Such payments usually begin within a few days after the bank closing.

With SVB, the FDIC saw itself having to avail and utilise a purchase agreement but also pay off depositors. I will talk more on this specifically in the SVB section below.

There was a fantastic story on FDIC taking over a bank and a segment on 60 minutes that shows what an FDIC takeover of a bank looks like. This might not be news to many of you but the FDIC is one of the few organisations that is held in high regards by the financial community/organisations around the world and has to a large extent mastered the playbook on how to put a bank into receivership and try to tackle the issues that plague the bank to the best of its abilities.

What does a bank really do?

I am entering a territory here that might warrant a lot of jeers/calls to correct/I don’t understand banking. I do not come with an absolutely strong opinion on this but nevertheless these are beliefs that I currently hold on what I believe a bank really does/what its role is. I am more than happy for anyone to message and correct me on anything I been incorrect on. I welcome that! :)

Here is an example of a thread from Frank Rotman at QED and in this specific example he highlights the theory that “deposits are lying around waiting for new loans to be originated”. This theory of money multiplier on deposits/deposits come first and are mapped to a loan is what creates a lot of confusion and in fairness a very common held belief. Nevertheless in my opinion, this belief is completely wrong and opposite of what actually happens.

I hope I am not misunderstanding him but this is completely incorrect. I even found myself questioning whether this has ever happened? As of 2020, Fed does not have reserve requirements anymore(See Fed policy tool page) and bank deposits can be moved to Central Banks if needed to build on reserves but it is not a common thing let alone what is highlighted above. This tweet also seems to conflate Central Bank Reserves with regular deposits. They are interchangeable if needed but not something that happens too often. For awareness purposes, UK where I currently reside does not have reserve requirements and and up until a few decades ago, Bank of England would work with banks individually to determine reserve requirements but that was scrapped as well.

I don’t mean to pick on Frank and only highlighting this thread as an example because it was widely shared. Hanlon’s razor which states “Never attribute to malice that which can be adequately explained by neglect” is probably what is at play here. This theory of deposits backing lending/money multiplier theory makes sense and is taught widely but there have been enough research papers(I will definitely write another post detailing this thought at some point) or commentary from the likes of economists/investors such as Steve Keen, Frances Coppola, Cullen Roche, George Selgin etc that have talked about how this is a fairly misunderstood concept and not at all how things work.

Leo Tolstoy once remarked “the most difficult subjects can be explained to the most slow-witted man if he has not formed any idea of them already; but the simplest thing cannot be made clear to the most intelligent man if he is firmly persuaded that he knows already, without a shadow of doubt, what is laid before him.” Let’s take the risk in hoping that I am not writing this only to have it fall on deaf ears :)

Banks have or do 3 main functions/jobs

Money creation(more implicit and not a direct mandate)

Maturity Transformation

Over the past century, banks have come to serve as arms of Central Banks and enable them to pursue its monetary policy(again, something implicit and what the situation has come to be)

Money creation

The money supply can broadly be classified as follows

M0 is ‘base money’ or the ‘monetary base’, sometimes known as ‘outside money’. It is the money created by central banks, or – in days gone by – governments. M0 is divided into two parts: physical currency in circulation, and bank reserves.

M1 is what most people regard as money, namely the money in their current (checking) accounts and in their wallets. It does not include bank reserves, because bank reserves are not ‘in circulation’.

M2 is M1 plus short-term savings accounts and overnight money market funds.

M3 is M2 plus long-term savings accounts and money market funds with a maturity longer than twenty-four hours. M4 is M3 plus other deposits. M1 to M4 are collectively known as ‘broad money’ or ‘inside money’.

All broad money, except legal tender notes and coins, is created by commercial banks.

It’s the highlighted part that I want to focus on because there were several comments I witnessed in relation to SVB crisis that made me really question how people think about what banks do and how money is created.

Money in its simplest form can be thought of as an IOU. People produce goods but simultaneously might want to consume someone else’s good. This is called coincidence of wants. Though, given the complexity of the system we find ourselves in, having coincidence of want or determining people who do is next to impossible task. Money therefore has come to surface and universally believed as the medium of exchange.

I remember, George Selgin in an eloquent manner highlighting how all of the misconceptions that people have can be classified under 3 buckets

(1) An ordinary bank must wait for reserves (deposits) to come its way in order to make loans; if they seem to maintain an 5% reserve ratio, then they can only lend 95% or deposits received.

(2) An ordinary bank can create money equal to a multiple of reserves (deposits) received. So if it receives X dollars and maintain 5% reserves, it can lend 20 times

(3) An ordinary bank can create money "out of thin air," with no need to either possess or to acquire funds by which to finance loans it commits to make, and hence no need to worry about either its actual reserve or the cost of securing funds from elsewhere.

In a very surprising way, during the SVB crisis, in some shape or form given how a lot of the issues revolved around deposit flight, I invariably saw commentary hitting exactly these 3 fallacies. People talking about how SVB couldn’t lend money because they don’t have deposits anymore or some saying, well they should be able to 10x the loans based on existing deposits. (Disappointed shrug)

Let’s try to break the fallacies apart and try to understand how things actually work.

How is money created if we focus from the perspective of the financial system that exists today?

Not from deposits. This is the prevailing theory of money multiplier/lending from deposits. In its simplest form, deposits do not beget lending. Lending begets deposits(this statement might sound preposterous but I promise to write an extensive blog post on this right after. This is not too relevant for SVB but it’s important enough to understand the reality of how money is created, what banks aim for, and what causes issues in the system to understand everything in this post)

Lets muster up an example - If I find myself looking for a £100 mortgage, I will walk over to the bank, present my case, bank statements, credit history and identification to begin with. Assuming that if the bank finds me to be a worthwhile borrower for the mortgage, they do not mandate the loan officer to look in the systems if there are deposits lying around somewhere in UK that have not been allocated. Not one bit. Banks have one and only one mandate. To grow their NIM which flows to their bottom line. This management of NIM is obviously done in keeping the risk-reward criteria in mind and staying within the capital requirements.

Net Interest Margin(NIM) =

(Interest earned on loans, fixed income investments in our AFS and HTM securities portfolios and cash and cash equivalents - Interest paid on funding sources such as deposits, CDs etc)/ Average Earning Assets

In having decided that I am a customer that meets their lending criteria, the bank in all essence is hitting a few keystrokes and creating two accounts on its balance sheet. The £100 loan is an asset for them and goes under the Assets side. As part of double entry accounting, they have to creating a counter account to the loan account. That is basically the deposit they create and money they have now handed to me. That is equal to £100.

That is it. In a very simplistic way, that is how money was created.

Now on the reserve requirement/money multiplier theory. I get how this might have been propagated as Federal Reserve used to have a 10% reserve requirement. The thing is that Federal Reserve abolished it in 2020. Bank of England does not have reserve requirements(for decades) and when it did, it worked with banks individually to determine what level of reserves it should hold. This money multiplier theory also doesn’t make sense given what I just highlighted above on how money is actually created and not contingent on some random ratio.

Finally, the money out of thin air commentary. In highlighting my example above, it very much does sound like it just appeared “from nothing”. Alas, there are constraints on banks lending and this is where the circle of lending gets completed. Remember how I defined money as an IOU. Well the deposit that the bank creates for my loan is an IOU from me on the bank. Deposits today are expected to be requested at will at any point and the bank is obligated(barring pre-agreed conditions) to hand those deposits over to me.

In this case, I am asking for a mortgage and in all essence have to hand over the money created to someone else who is selling me the home. There is a very good chance that this person does not bank with my bank and therefore the £100 is taken out of the account and deposited in the sellers bank account. This is where problems originate depending on the liquidity situation of the bank. The lending bank must have enough Central Bank Reserves(every bank holds reserves with Central Bank) to finance this deposit transfer. You can click a few buttons and electronically say that the money is moved but at the end of the day, settlement needs to happen. This settlement happens between banks via Central Bank Reserves.

When the loan is created, the bank need not have these reserves but when settlement happens, it does need to have it. If it doesn’t, it either can borrow via interbank lending, via gaining deposits from someone else, via borrowing from Central Bank. Therefore think of deposits as one of the ways by which a bank provides liquidity to settle a transfer. That’s it. Liquidity management and having reserves to engage in it is at the core of what happens and what deposits are really needed for.

Therefore, the banks cannot just continue to create loans because for every loan created, there will be a deposit created. A deposit is an IOU on the bank and if there is an understanding in the market that the bank is providing loans in an unprofitable manner or creating too many loans, whoever gets the deposit will work their way into taking it out, creating a liquidity crisis, and causing the bank to close. Think SVB(obviously when it comes to liquidity crunch and not the bad loan part. More on this below) :)

Maturity Transformation

Having solved the problem of how money is created, let’s extend this to what happens after that. In a complex world of financial services with thousands of banks, deposits moving across all these banks as consumers of deposits buy services and pay others, this means that there is an imbalance of the loans that the bank has generated vs the deposits it might find itself holding.

I talked about how Net Interest Margin is the core of what the bank is focussed on. Deposits being IOU of the banks can be called upon at any point and hence are very much short term liabilities of the bank. There are ways where this can be turned into long term by locking away deposits via products but let’s ignore that for now. On the Asset side, especially as we consider loans and mortgages, in U.S 30 year mortgages are the norm. Loans in general are much longer in duration.

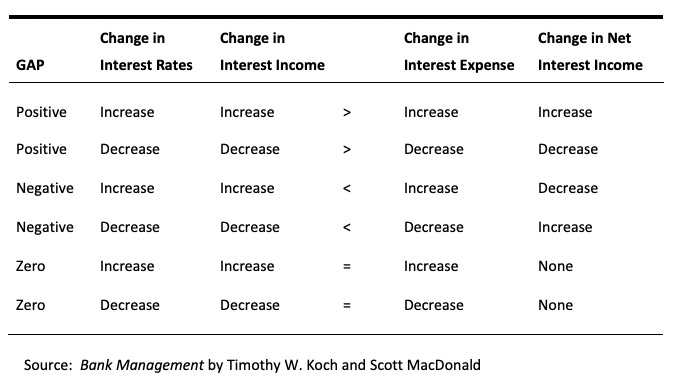

Maturity Transformation therefore is an inherent feature of the banking industry. They invest in long term loans which are assets but on the opposite side of the balance sheet, find themselves funding these via short term liabilities. The biggest risk in engaging in such a business is the interest rate risk that comes with the duration mismatch. Managing that is what bankers get paid for!

Banks have come to serve as arms of Central Banks and enable them to pursue its monetary policy

I don’t profess to know how the financial system works across every country and therefore in keeping a U.S/U.K centric view on this, Central Banks have several levers(raising/reducing rates, increasing/decreasing central bank reserves, purchasing assets etc) that they pull/push upon to engage and accomplish its monetary policy. The conduit via which this is accomplished are the banks. In U.S, this only happened post creation of the Federal Reserve in 1913.

Understanding SVB and its business model

To make any business work, you in essence need an idea, ability to execute, access to talent, luck, and most importantly funding. It was in providing this access to capital and other banking services that allowed to SVB to position itself as a critical player in Silicon Valley. The origin and location of SVB has no randomness to it.

Having started in 1983, the firm was the brainchild of 3 people(two Wells Fargo bankers, Roger Smith and Bill Biggerstaff, and a Stanford professor, Robert Medearis). In looking at the tech ecosystem at that time(IBM, HP, Apple, Microsoft, Intel, Sun Microsystems etc), they realised that this was most likely a secular trend where Silicon Valley would see the proliferation of new startups with most of the funding coming from VCs and having someone to understand the needs while providing banking services was the key.

Startups especially in its early stages(broad assumption but let's go with it) either are not profitable or have even figured out how to make money. For a traditional lender, startups as a whole did not fit neatly into their risk models and therefore were leaving these set of customers behind when it came to providing lending facilities. SVB realised that their core advantage would come from understanding the needs of these startups, finding diversification by targeting firms across different verticals, and building relationships/services to help these firms from inception to when they went public.

Over the pursuing decades, SVB continued to build out new business lines that integrated it deeply into the tech/healthcare startups ecosystem but a key decision that the firm took to complete the cycle of integration was also providing the same services to the VCs. In becoming the banker to the VCs, they firmly implanted themselves in the middle of the financial flow between the two players. Another critical service that turned out to be important in courting VCs was providing what is called capital call loans.

When a VC or PE fund raises money, it typically raises in the form of commitments, and has to actually request the money before making an investment. Capital call loans are essentially short-term loans collateralised by the promise that fund investors will make good on their commitments. At one level, this is a very trustworthy loan; at another, though, there's a lot that can go wrong in the interpretation of an elaborate fund agreement. By making these loans, though, SVB is also improving the value of collateral for their higher-risk loans; funding rounds are more likely to get done when they can get done fast, and capital call loans ensure that this can happen.

To highlight how stickiness was created, let me highlight via an example - Startup “A” raises money from VC “B”. This transaction would involve a flow of funds from VC “B” to Startup “A” with each of the firms having their own banking providers. SVB over the decades built strong relationship with the VCs and through these relationships coaxed them to encourage the startups they funded to also bank with them. The benefit of doing so came in the form

SVB providing lending to these startups in lieu of them bringing all their banking needs and deposits to them.

Provide venture debt that was added on top of the equity financing that the startup might have raised

Continue to meet the needs of these startups as they went through their growth stages

Increased trust, built a network, and provided other intangible benefits to both VCs and startups

SVB from what I have been able to figure out was probably amongst a very few set of banks especially amongst the early stage startups scene to also hold warrants on the firms. These warrants came via the venture debt and in their last annual report, they highlighted holding ~3000 warrants in startups

Below is a snippet from a post about how SVB was able to lock in Startups/VCs with its services

SVB offered banking services to startups that often weren’t profitable, in some cases didn’t even have a product, and would otherwise have a hard time getting a line of credit or a loan from a larger bank. Venture-capital firms banked with SVB too, often encouraging their portfolio companies to do the same. Mo Parikh, founder of software startup Bandwango, switched his company’s accounts over to SVB last year because his company wanted to get a line of credit and SVB’s terms were attractive. Bandwango took out a $1.5 million line of credit in exchange for doing all of its banking with SVB and giving the bank warrants. SVB was lenient when it came to underwriting loans, according to founders and investors, which allowed the bank to dominate the venture debt business and underwrite transactions that larger banks deemed too risky. SVB also had an army of relationship managers that wooed their founder and investor clients with personal service, driving business. The bank also offered invitation-only mortgages to company founders and venture-capital executives.

What was SVB able to achieve in providing these services and building upon this strategy? Since inception and over the next 4 decades, SVB managed to build atleast a reputation for the bank to work with in both the VC and startup community. Based on their most recent public filing, SVB worked with ~3300 VC/PE firms(including some of the biggest/prominent VCs in U.S).

Source - SVB financial reports

Source - SVB website

and banked almost half of the VC/Life sciences startups in U.S

Source - SVB financial report

SVB like other banks has always had complaints on the services being provided, interface, time to open account but a key thing to consider that plagues every organisation is “you can’t be everything to everybody”. My understanding and in researching for this post is that a lot of complaints stemmed from pre-seed startups/seed stage startups or corporate banking providers. I don’t have insider info on but it could be that if we take a view of the potential customer base, these two type of firms are probably in the low prioritisation area of the customer base that they truly focus on.

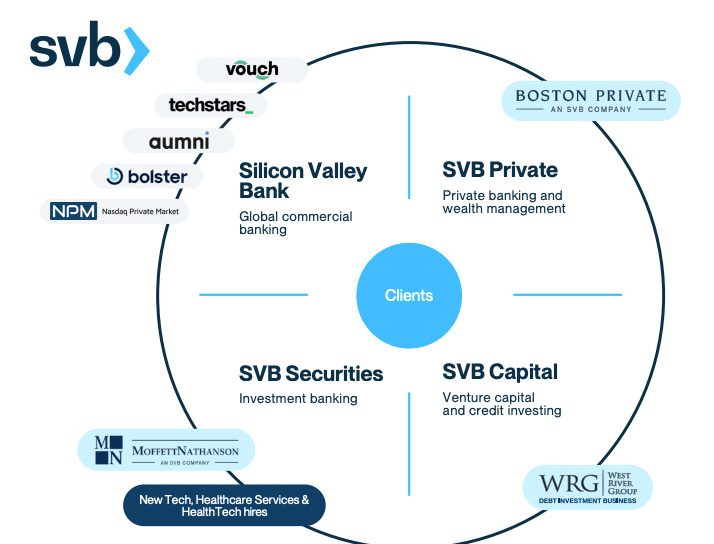

If we actually look at what SVB offered, they had a fairly extensive suite of products it was providing to clients across the Tech/Life Sciences startups and across various stages from inception to public company.

Source - My attempt at being creative

If one double-clicks by the type of customer that they were catering to, the product suite and their positioning becomes even clearer.

Examples of features offered for early stage startups -

Local Banking services -

Checking/current account

For early stage startups, up to 3 years of free checking account services. Post that $50/month + fees on payments

Wires - incoming and outgoing (USD domestic and international, FX)

Remote Deposit Capture for scanning and sending electronic images of checks directly to SVB from your desktop

SVB Direct Connect - Connections to Quickbooks, Xero, Expensify and other authorized applications

SVB TransactGateway for payment automation through back-office accounting software or ERP.

Payments and business cards

Debit and credit cards

Unlimited rewards

Global Banking

Multi-Currency Account (available in 19 currencies)

Certificate of Incorporation

EIN - US Company Tax ID

Global Payments and Foreign Exchange -

Send and receive payments in 90+ currencies in over 110 markets around the world

Foreign Exchange

Forward contracts

Swaps

Hedging

Options

FX Risk Advisory and strategies

Global trade finance

Liquidity Management

Money market account with a competitive APY of 4.50%

Cash sweep programs(Blackrock, Morgan Stanley, Western Asset management)

Lending

Examples of additional features(everything above included) offered for venture-funded startups -

Venture Debt

SVB Private Banking(especially for founders and senior execs)

Wealth Management

Private banking

Investment Advisory

Examples of certain features offered for late stage private and public companies -

Global Banking

Investment Banking

Credit and Capital Solutions

Examples of certain features offered for VC/PE firms -

Advocacy and Advisory

Network and Industry Connections

Proprietary data/knowledge platform

Global Customer Service Team

Source - SVB annual report

Over the past 2 decades, SVB took this playbook/product suite and expanded not only across different life stages of a startup but also several countries with UK, China, Israel, and Germany being at the core of its focus especially given the tech ecosystems in these sectors/countries.

Source - SVB annual report

Source - SVB annual report

View on U.S economy/fundraising post GFC(Great Financial Crisis)

Before I specifically look into the events that culminated in the collapse of SVB on March 10th, 2023, I want to broadly look at the state of our financial system/economy/central bank policies post-GFC. In understanding what I believe was the natural state of things

The 2008 crisis saw 3 main things emerge that laid the foundation for the next decade

The ZIRP(Zero interest rate policy) especially across U.S/EU Central Banks.

There were rate hikes post 2015 but that stopped in 2019 with the repo crisis and freezing of the markets. That in turn forced the Fed to engage in QE starting 2019 again

Quantitative Easing and asset purchases by Central Banks

Regulatory changes

The 2010s saw significant increase in private company financings/M&A/IPOs as well as massive run up in equity valuations especially in the U.S markets. 2010s saw the U.S market outperform the Emerging markets.

Reason for run up in equity valuations can also be explained by what valuation is in its core essence. It is taking the expected cash flows in the future and discounting them back to the present. Discounting back is happening based on the discount rate. There is no such thing as a discount rate that everyone uses and is usually at the discretion of how someone making an investment might think of it. One way to potentially look at discount rate is to look at risk free rate(in U.S, this would be the interest one can make by investing in treasuries.). With rates almost at 0 and discounting back the cash flows with low rates means that the valuation of a company would be higher.

The second order effect of low interest rates was in everyone trying to determine potential investment opportunities where they could make higher returns. This was especially evident in the way pension funds were increasing their fund allocation to alternative assets(VC/PE/Real Estate etc).

With the onset of covid in early 2020, there was a massive increase in fiscal and monetary stimulus especially across U.S/EU.

All combined, 2021 saw massive run up in equity valuations, money deployed via venture capital/private equity, and increase in asset prices(especially real estate) across the board.

Covid lockdowns had a massive impact on the supply side especially considering China shutdowns in 2021.

These trends were pretty much universal across most of the countries.

2022 finally saw the confluence of many things -

Supply chain issues

Inflation that was deemed transitory initially but really turned out to be sticky and way past what the Central Banks felt comfortable with

Russia-Ukraine war

Rate hikes(almost all the Central Banks engaged in this)

Beginning with inflation in U.S, post 2008 Great Financial crisis and onwards, inflation usually hovered under or slightly over the 2% mandate that the Federal Reserve usually targets.

Confluence of factors ranging from supply side shocks given Covid closures, fiscal relief during covid, zero interest policy, and finally the Russia-Ukraine war led to inflation climbing up to a peak of 9.1% in 2022.

Beginning of March, 22, Fed has raised the Fed Fund rates by 4.5%.

As you can see from the chart below, this is the 3rd fastest rise in rates(early 80s and early 70s being the other two time frames that I am talking about)

What transpired over the past year and on the fateful week of March 6th?

Reading the hysteria/conversations on on twitter and looking at the VC crowd during the SVB crisis reminded me of Gary Oldman in True Romance saying “we got everything here, from a diddled eyed joe to damned if I know”

For all the shortcomings, my goal here is to not sit and rip apart the statements made during that 1 week period. Hindsight in my opinion tends to lend rationality to events that in fact are innocent of coherence or logical sequence.

If I have to absolutely simplify it, SVB went into FDIC receivership because of liquidity issues caused by the bank run.

Not to make light of the situation, Robin Williams making fun of the banks wanting liquidity in the Great Financial Crisis was what was in essence the biggest problem that SVB was facing(temporarily). One thing I have been looking in relation to SVB has been the tech bubble and how it withstood the crisis. The fall out of grace and losses it faced back then were greater(potentially a separate post) but the key difference was that the economy back then was not coming off of a 12 year near 0% interest rates to ~5% now given the hikes.

The best way I believe to approach the issues that plagued SVB is to work across the balance sheet from the Liability side, glancing at the asset and the way management diversified across various opportunities, and finally bringing it all together to understand what happened on March 9th/10th for it all to go wrong for SVB.

Liabilities

In the simplest form and for the purposes of this conversation, liabilities for a bank is some combination of the deposits it holds on behalf of the customers and shareholders equity(considered non-money)

Deposits as I highlighted in section on what a bank does is really an IOU of the bank held by consumers, businesses, enterprises etc and expected to be available on demand(unless you have deposited in mid-long term CDs or other products that the bank offers).

SVB was a bank predominantly for the startup/VC ecosystem and a bank that grew enormously but not in a surprising way if we consider the growth and importance of Silicon Valley over the past 40 years. From having a wallet share of the VCs that was near 100% in early 1980s, Silicon Valley and the startups that inhabit that ecosystem still garner majority share of the dollars invested every year.

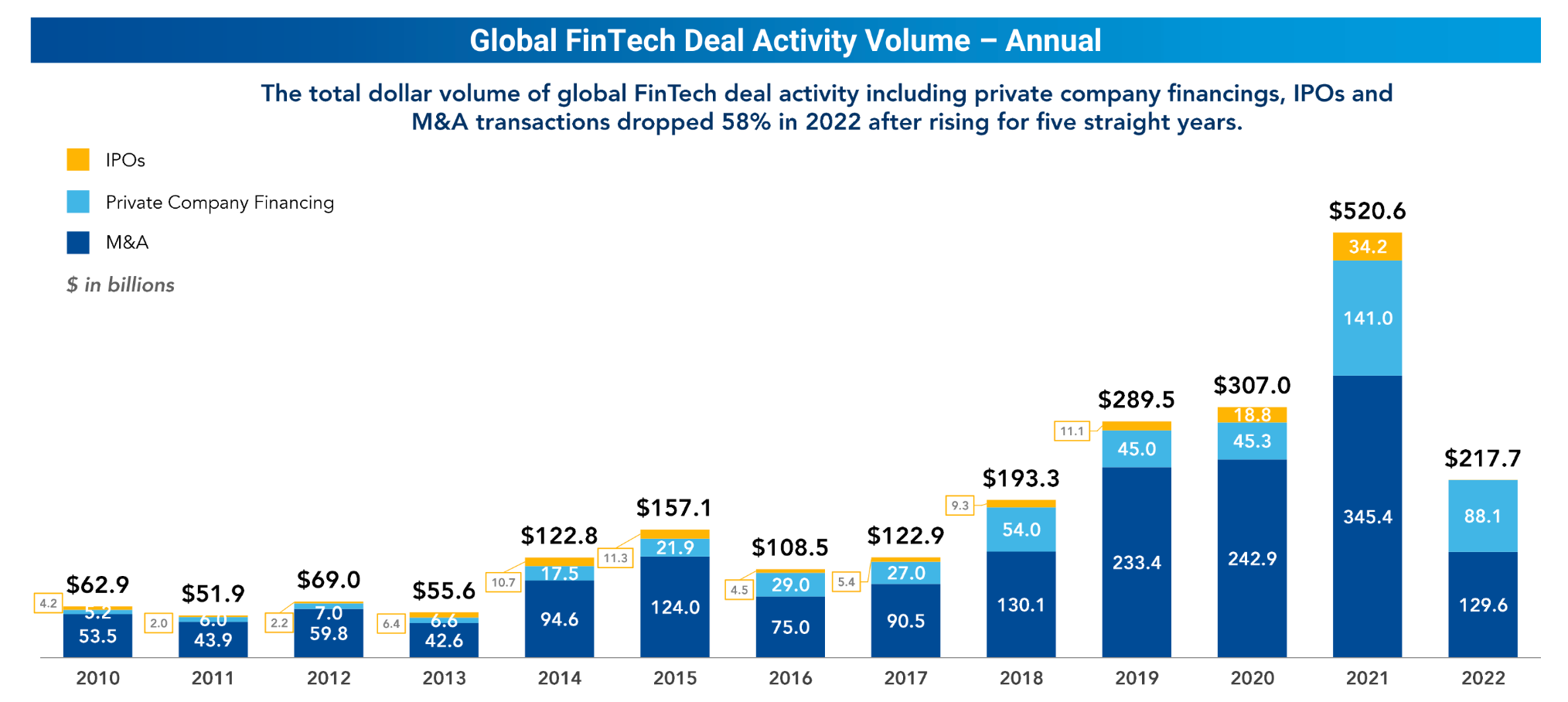

This is very specific to FinTech as this was easily available and the only view I could find going back a decade but you can see the progression of financing over the past decade. From what seems like a paltry ~$63B in 2010 to $520.6B in 2021 which we can with all certainty deem as the end of the era of easy money that got kicked off post GFC.

Source - FT Partners

A thing to remember is that as much this post is of how things panned out in U.S, the glut in availability of capital and investments into startups was a global phenomenon. SVB in turn was one of the biggest beneficiaries of this trend more so over the last decade than any decade before in its existence.

Source - SVB annual report

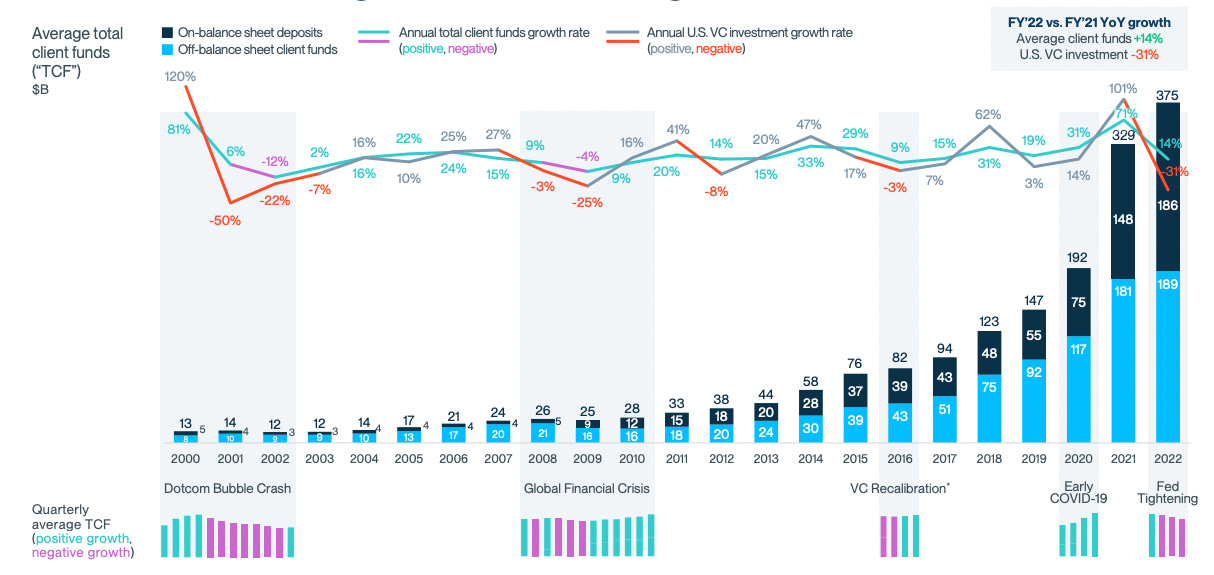

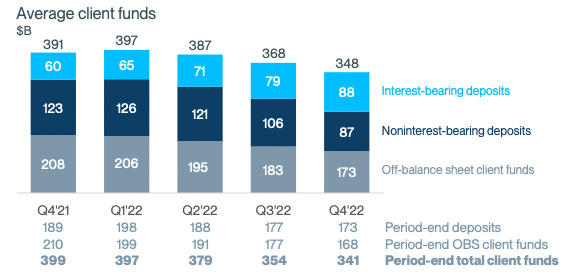

Growing from $28B in client funds on the liability side of the balance sheet in 2010 to ~$375B in 2022 is a mind boggling growth when we thinking of a bank. Hindsight is 20/20 but this massive growth in deposit base from predominantly their VC/startup customer base should have raised a few alarm bells.

The 2022 VC investment drop(don’t believe the chart above considers Q4-22) was roughly in line with the VC investment crash post dotcom bubble yet, SVB seemed to have survived that crash without a deposit flight. I reckon the reasons are -

Late 90s was a time frame when the interest rates set by Fed were nowhere close to the 0 bound that has been the norm over the past decade and a half. That meant that it was fairly common for banks to offer decent rates on deposits thus creating some element of more security in ones ability to retain them.

Despite the reduction in VC investment, 2001-02 time frame saw decreasing rates given the recession/9-11 vs what banks are having to deal with right now with reduced loan demand, losses on the asset side of the balance sheet, increasing pressures on deposits and thus a negative impact on Net Interest Margin(NIM).

Late 2020 and for all of 2021, with fiscal stimulus and massive easing in monetary policy in full force, SVB saw the largest inflows in deposits from all the fundraising/SPAC/IPOs that were underway in the broader market. Greg Becker who was the CEO of SVB in the latest quarterly highlighted the following

When you look at the last four or five quarters we've seen rapid growth in quarterly venture capital flows and that's the biggest catalyst of deposits for us.

Chuck Prince who was the CEO of Citi prior to the GFC is reported to have said “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing,”. I figure Greg Becker wasn’t necessarily thinking the same way and probably expected to be retired one day, sitting with his grand kids and telling them the following story

Source - An amazing freelancer on Fiverr

well kiddos, we primarily banked startups/VCs —> they did really well especially after I joined in 2011 —> we provided pretty much anything and everything in terms of services and were well regarded in the ecosystem —> We grew too fast and were slightly worried. —> Made some tough decisions on how we invested the money and crossed our fingers when things went a little bit south —> Something happened in the middle that no one knows since this is fictional story —> SVB turned out to be fine and I passed on the reigns of a storied brand to someone else

Alas, that is not how the story ended as we know.

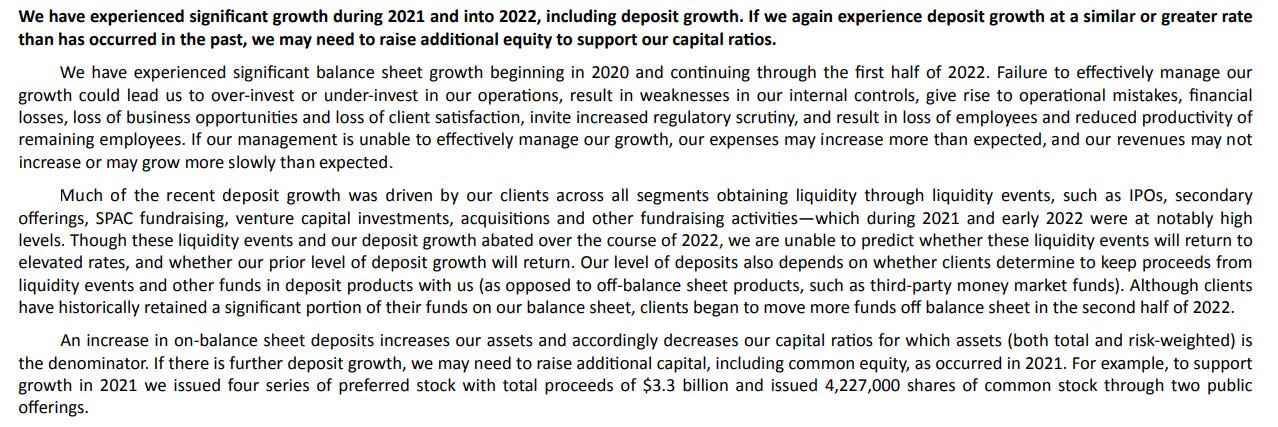

Now in all fairness, deposit growth and the risk around is mentioned very clearly in the annual report though very much from the perspective of what impact does it have on the capital ratios

Source - SVB annual report

The monetary and fiscal stimulus which directly had an impact on fundraising/valuations and benefited SVB tremendously would also be the reason for the downfall. As inflationary pressured picked up and rather than it being transitory which was the talk of the town in late 2021, cementing itself in a more permanent way meant that the Central Banks found themselves having to take aggressive measures to curtail the growth of money supply and started hiking rates. Combining with the Russia-Ukraine war, the end of easy money policies led to drastic slowdown in all deals. Below is an example from the Fintech side of things but 2022 saw value of all deals(IPO, private financing, M&A) fall to $217.7B which was a ~58% reduction compared to 2021.

Source - FT Partners

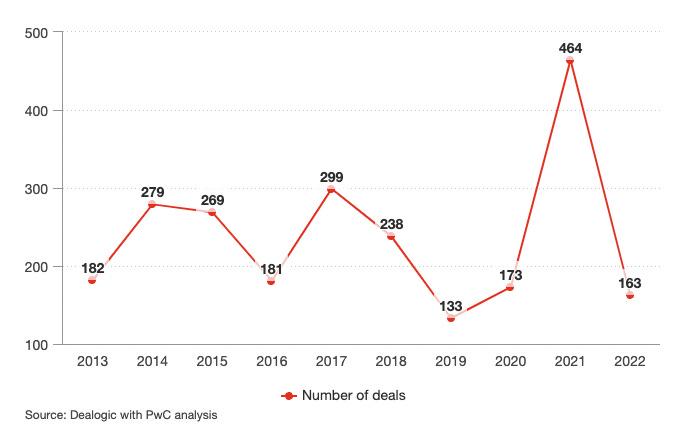

If we look at the IPOs, U.S and Europe saw massive drops in the number of IPOs in 2022 and reverted to being slightly lower than the 2018/2019 numbers.

Source - PwC - U.S.A IPO deals - 2022

Source - PwC - Europe IPO deals - 2022

SVB did have presence in APAC saw a slight slowdown as well but the reason for the resiliency lay in IPOs happening in China, South Korea and India. China saw the highest number of IPOs over the past 10 years and the $ volume raised was elevated because of China National Offshore Oil Corporation and China Mobile listing on the Shanghai stock exchange after getting delisted on NYSE in 2021.

Source - PwC - APAC IPO deals - 2022

The reverberations of a fundraising environment that was tightening up started to make its way through to SVB and its liability management in 2022. Here is an excerpt from the last quarterly report in regards to what the team was noticing with deposit flows

The decrease in deposits of $16.1 billion compared to December 31, 2021, was primarily driven by slowdown in public and private fundraising and exits as well as increased client cash burn, partially offset by flexible liquidity solutions that shifted off-balance sheet client funds on-balance sheet, all of which reduced the proportion of noninterest-bearing deposits.

I absolutely love the insights that the team was able to gleam in the deposit outflow and in mapping it to the client/fundraising, they figured that the problems that were emanating around the deposit outflow was because of cash burn at startups at levels similar to 2021 time frame.

The lack of fundraising/cash burn was probably the most important reason for reduction in deposits on the balance sheet. The second factor and what was becoming an ever growing issue was the growing awareness amongst customers around the possibility of earning interest on their deposits. This is the battle that banks are having to engage in and broadly the argument is contingent on what you believe your deposit beta is, what level of competitive pressures are you facing and how unstable your deposit base is(depending on how many retail customers do you have vs large deposit holders vs concentrated bet on an industry).

Source - SVB annual report

SVB especially towards the tail end of ‘22 when the rates were really picking up saw itself starting to increase the rates and movement of more and more deposits into interest bearing accounts. The estimate from the management was that with almost fair certainty, the trend was going to continue to pick up especially given the fact that the average amount in an account at SVB hovered around ~$5M. Barring obviously the uninsured part, that is a significant amount from a treasury management perspective to be sitting around earning bare minimum when you have multiple options especially in the form of MMFs to earn money on cash sitting around.

Assets

Broadly, this side of the balance sheet for the bank predominantly revolves around the loans it originates though the banking industry is fairly complex and deposits move around.

Source - SVB annual report

For SVB, only $70B out of the $216B amounted to the loans it originated. The majority of its assets were actually in investment securities which we will touch upon below. Double clicking on loans, we see that ~60% of the loans had a tenure outstanding of less than 1 year. This in my opinion highlights that that SVB had the opportunity to originate lending(this is obviously contingent on the assumption that the macroeconomic situation doesnt take a turn for the worse and there is demand for loans) and account for the rate hikes that have taken place over the past year.

Source - SVB annual report

I say this with some certainty because we actually saw this play out for them according to their latest quarterly reports. Mind you, this is a significant increase in average loan yield considering that it was only across 1 quarter.

Source - SVB financial report

If we look at the quality of the loans being made, based on the data provided by SVB, it looks like that the loans were performing as expected and the bank had not really seen any adverse impact despite the rate hikes.

Source - SVB financial report

The problem in my opinion wasnt necessarily in their loan portfolio but in the investment securities and how they managed the duration risk. Before we look in detail what SVB management was really doing it is important to understand what Held to maturity and Available for Sale really means. I don’t wish to opine on what the accounting standards should be and how should banks go about doing this as that is outside my payscale and understanding but if anyone wishes to get into the technicalities, PWC has details available over here

Now broadly, Held to maturity are debt securities where the intent of the bank holding on has an intent and also the ability to do so until maturity. Available for sale are securities that the bank may retain for long periods but that may also be sold.

Federal Reserve a few years ago put out a report on the changing nature of HTM and AFS securities across all the banks in the U.S

Source - Federal Reserve

Source - Federal Reserve

We can see that post-GFC, given the regulatory changes and focus on building up the capital base and ratios of the banks, there was an increasing shift towards Agency MBS. I was not able to find a similar view up to 2022 but in taking a quick glance at the recent data(see table below), MBS now account for nearly 10% of the assets of commercial banks in U.S.

Source - Federal Reserve data

Byrne Hobart did a fantastic write up explaining the rationale behind agency MBS which as we see above have become a significant part of the balance sheets of banks

US financial regulations have spent a century-plus trying to deal with three interrelated facts:

Banks are a great way to aggregate lots of capital.

The single greatest demand for capital comes from mortgage origination. (Equities are a bigger market, but mortgage origination is an order of magnitude higher than annual IPO volume.)

While banks are natural participants in the mortgage-origination process, they're not the ideal holders of mortgages, because banks fund their balance sheets with demand deposits, and mortgages are hard to liquidate on demand.

The agency paper market exists to partly solve this problem. The basic idea is to remove two of the complicating features of mortgages: the risk that the borrower won't pay the mortgage back, and the fact that a single mortgage (or even a portfolio of mortgages) is an incredibly inconvenient thing to sell.

It works like this: quasi-government agencies (Fannie Mae and Freddie Mac) or an actual government agency (Ginnie Mae) buy up residential mortgages that conform to certain criteria. Then those agencies create financial products that are tied to the payback of the mortgages—but insured against defaults—and sell them as mortgage-backed securities (MBS) on the agency paper market.

Finally, in a hyperbolic way and something to keep in mind as we look at the portfolio and understand what happened at SVB, when interest rates go up, the current bonds that are outstanding will see their value go down. When interest rates go down, the current bond holders will see the prices of those bonds go up. The technical reason behind this has to do with discounting the cash flows using the current interest rates vs what was originally offered and getting the present value of the bond from that analysis. The qualitative reason is if you currently hold a bond that offers you .25% and the interest rates go up to 4.75%(which they have), there is an opportunity cost for you to continue holding on to that bond or for anyone else to do so if you try to sell them that bond. Therefore, to compensate the person for ignoring a 4.75% bond that they can buy means you will have to sell your bond holding at a cheaper price to account for the opportunity cost and incentivise them to engage in the trade.

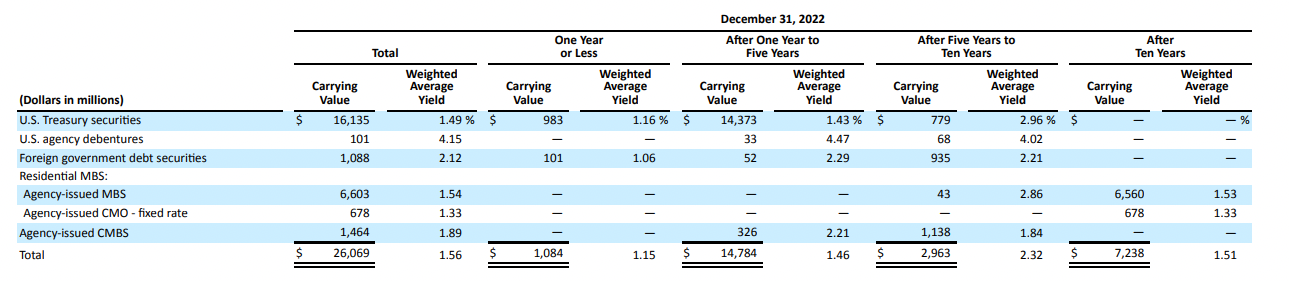

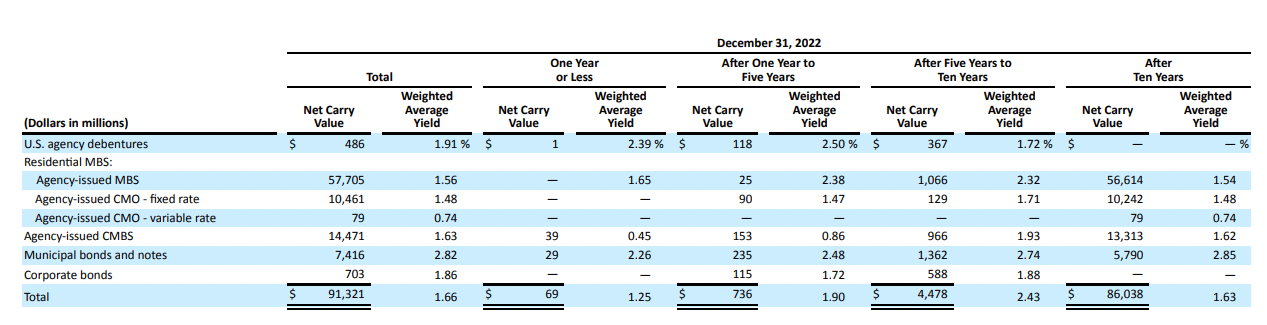

Similar to the loan portfolio, what SVB was holding in its investment securities portfolio and the quality of it is not really the issue. As you can see, it was predominantly U.S treasuries, agency issued MBS, and agency issued CMO(collateralized mortgage obligation).

Source - SVB annual report

The issue was very much in the duration risk surrounding the the investment securities and the decisions that the bank and its management decided to take in 2022.

Source - SVB annual report

Source - SVB annual report

Below is an excerpt from their financial reports on how the duration of their investment portfolio increased

The estimated weighted-average duration of our fixed income investment securities portfolio was 5.7 and 4.0 years at December 31, 2022, and December 31, 2021, respectively.

The weighted-average duration of our total fixed income securities portfolio including the impact of our fair value swaps was 5.6 years at December 31, 2022, and 3.7 years December 31, 2021.

The weighted-average duration of our AFS securities portfolio was 3.6 years at December 31, 2022, and 3.5 years at December 31, 2021.

The weighted-average duration of our HTM securities portfolio was 6.2 years at December 31, 2022, and 4.1 years at December 31, 2021.

It is absolutely baffling that in 2022 as rates went from .25% to 4%, the management rolled over existing investment securities and any additional money into longer duration investments rather than pursuing a risk averse strategy in uncertain times. These decisions were not just taken in 2022. The move towards longer duration securities started in 2020 as the team trying to figure out how it could invest across longer duration securities to make any additional interest income it could to juice up its profit. At that point, rate hikes were not even a remote possibility.

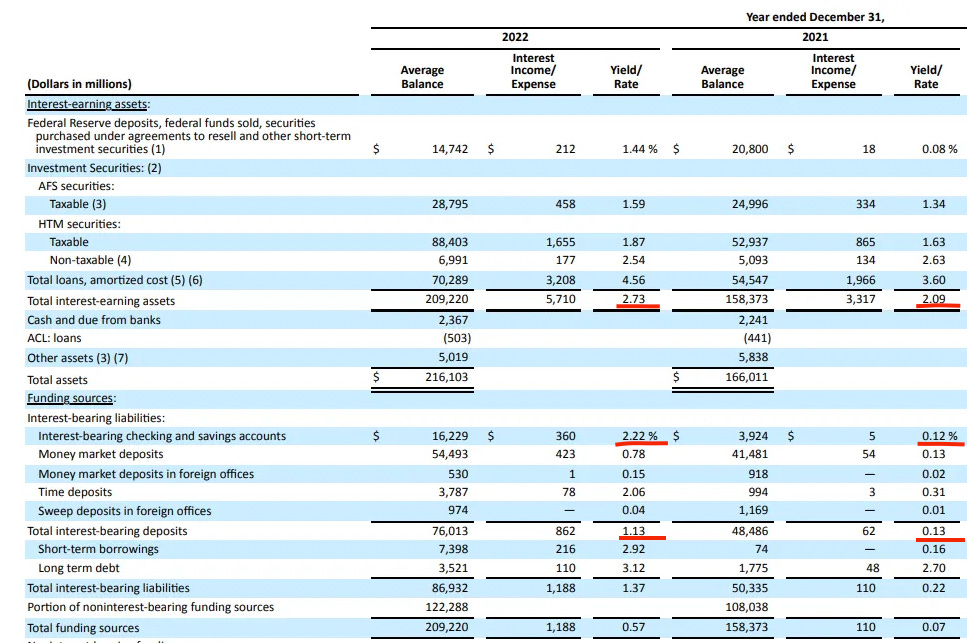

It might seem bone-headed when looking back but if we look at change interest rates across their asset and liability side, I can somewhat see what might have prompted the SVB management to invest across longer duration securities.

Source - SVB annual report

I have highlighted the line items that I believe are the key especially from the viewpoint of how NIM gets affected. In a span of one year, the interest expense for SVB on customer deposits increased by 1% whereas the interest income on assets only increased by .64%. This has a direct impact on the profitability of the bank and if your compensation, how you are judged in terms of performance, maintaining capital ratios etc is dependent on continuing to be profitable, this is a worrying trend.

Therefore the firm decided to continue adding to its long term securities and estimated that the rate hikes would pause and also go down given their views on inflation not being too sticky. Well, how wrong did that belief turn out to be.

Unraveling of SVB

It is always hard to pinpoint to an exact moment when things started going wrong with SVB though one thing is clear, it wasn’t a complete surprise as people make it out to be. The regulators had highlighted potential risks around SVB and after the last quarterly report in January, there was a fantastic twitter thread on SVB that highlighted very much the potential issues that lay before SVB. Byrne Hobart towards the tail end of February also talked about the issue around leverage and the HTM securities.

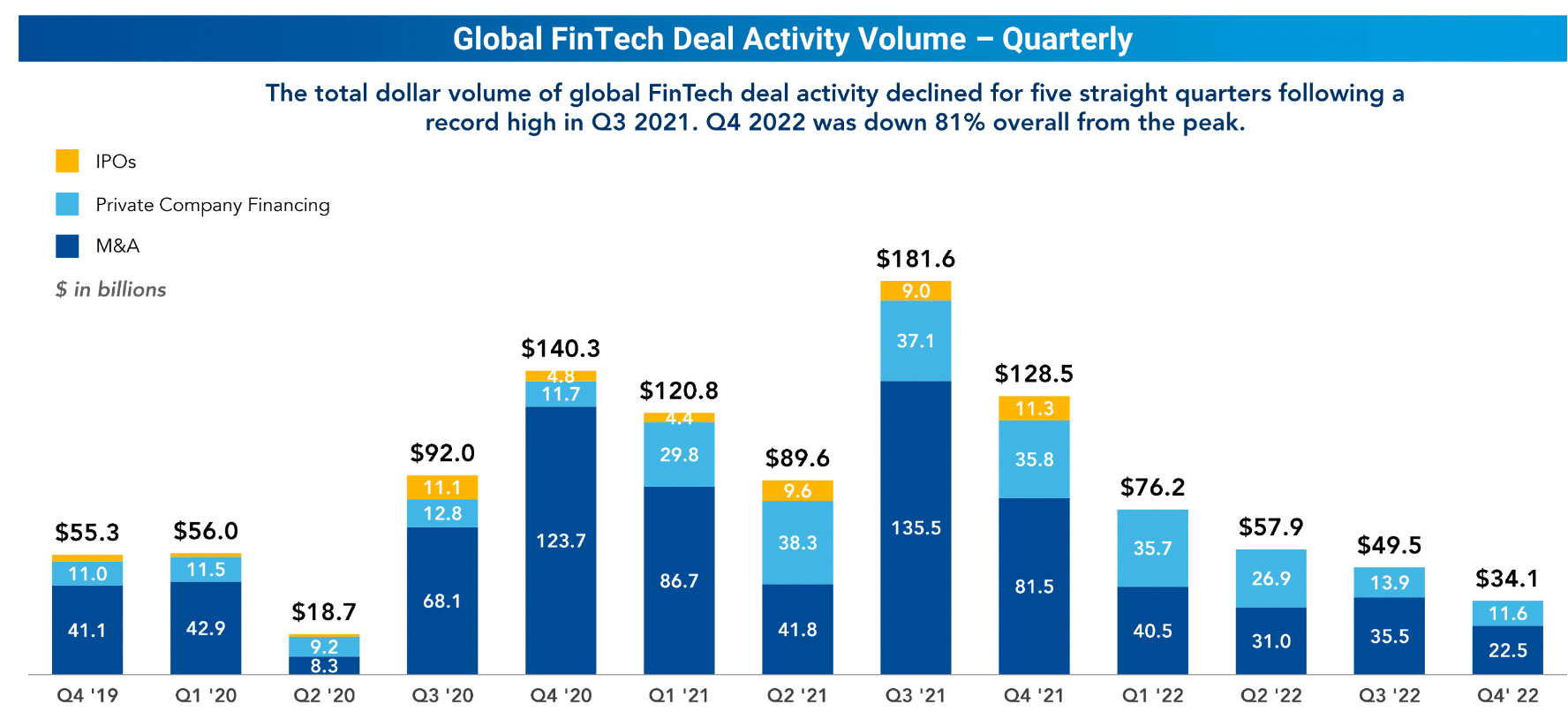

I talked about how the combination of inflation + rate hikes has led to a significant reduction in fundraising/IPOs in the startup community. With this reduction and the cash burn that remains elevated, SVB started seeing a significant pull out of deposits from its customers. The chart below shows that in 2022, SVB saw nearly ~$60B in deposit outflows.

Source - SVB strategic review

Usually in expectation of such deposit outflows, banks keep liquid securities/cash available but $60B meant that SVB had to start looking its securities portfolio and make determination on what needed to be sold to meet these deposit calls. Over the past 2 years, I highlighted how the duration of the investment portfolio had significantly increased

The weighted-average duration of our AFS securities portfolio was 3.6 years at December 31, 2022, and 3.5 years at December 31, 2021.

The weighted-average duration of our HTM securities portfolio was 6.2 years at December 31, 2022, and 4.1 years at December 31, 2021.

Therefore, with these deposit requests coming in and with the investment portfolio facing losses given the rise in interest rates, the bank was facing a situation that was only becoming more stressful. The ratings agencies despite being late to the game realised what predicament SVB was finding itself and were planning on downgrading the banks rating and did highlight this to the executive team in the beginning of the week of March 6th. Over the next couple of days, the bank made a critical decision and published their actions in the Q1,23 update

At the core of it, the bank did the following -

Sold $21B in AFS securities(all of it) and recorded a $1.8B loss.

Given the pressures they were already facing on their Return on Equity, SVB would try to raise $2.25B in common equity and preferred shares. Also got General Atlantic to commit to $500M.

These actions were taken because the bank grew more confident in the fact that the interest rates were not going to be falling down anytime soon, and the cash burn and thus the deposit outflow from startups would continue.

It is reported(though I don’t want to give air to who did what and how dare they do it) that VCs upon hearing about the potential losses and liquidity issues at SVB asked their own teams and the startups they had funded to take out whatever they could beyond the $250K in FDIC insurance that is applicable for an account. Now, assuming that there was this request made, I personally don’t find any issues in deposit holders watching out for their own interests and protecting their deposits by moving it to what they perceive to be safer. It is absolutely irresponsible to question/call someone out for having recommended this because it shows a lack of understanding of fear/basic human psychology.

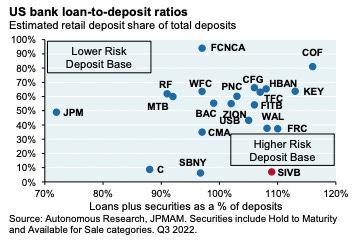

Also consider the following about SVB. Nearly ~90% of the deposits held at SVB were uninsured which means they were above the $250k limit that FDIC currently has

Combined with the concentration of the types of customers(see chart above) SVB had(VCs, healthcare, tech companies), it was only inevitable that once the news around the viability of the business started spreading, there was going to be a panic.

That was exactly what happened. An initial flow of deposit that had led SVB to sell assets/take losses only accelerated and on Thursday(march 9th), the firm saw nearly $42B in deposit outflow which led to a liquidity crunch on Friday(10th of March). The FDIC which was most likely going to close the bank on Friday evening post business hours realised the severity of the situation and put SVB into receivership early into the day itself.

Source - me

SVB was the 2nd largest bank bankruptcy after Washington Mutual which went bankrupt in 2008 and was acquired by JP Morgan.

Over a period of 2 and a half days, a lot happened and I dedicate a whole section below on the responses by other fintechs in terms of launching products/thinking about how to serve the SMBs/startups that were affected because of the SVB crisis. In essence, there were 3 questions that everyone was really trying to answer and assign probabilities to -

Will the FDIC be able to find a buyer who could guarantee the deposits and stem the flight of customers?

If no, would they along with Fed and Treasury try to guarantee part/all of the deposits to prevent chaos from spreading across the financial system?

For customers who banked with SVB and had not been able to take their money out

The initial view came from looking at FDIC reports and how things had panned out over the past 4 decades

The general idea is that in bankruptcy, from a legal point of view, people get paid back based on a waterfall method where the seniority is clearly defined. The insured deposits, FHLB, and Fed are first priority and then comes uninsured deposits, senior debt, other debt, and equity.

Slight digression here but one of the agencies that goes under the radar but is critical as the second to last lender of resort in U.S is FHLB. More on them below

FHLB - The Federal Home Loan Banks (FHLBs) are a system of regional member-owned corporations that provide lending institutions with a liquidity resource to finance housing and economic development activities. Congress established the Federal Home Loan Bank system in 1932 as a government sponsored enterprise to support mortgage lending and related community investment activity in the wake of the Great Depression. The FHLBs’ mission is to provide reliable liquidity to its member institutions to support housing finance and community investment. While the FHLBs’ mission reflects a public purpose, all FHLBs are privately capitalized and do not receive federal funding. Unlike the other government sponsored enterprises, Fannie Mae and Freddie Mac, FHLBs do not guarantee or insure mortgage loans. Instead, FHLBs act as a “bank to banks” by providing long- and short-term loans known as “advances” to their members, as well as specialized grants and loans aimed at increasing affordable housing and economic development. In some cases, FHLBs also provide secondary market outlets for members interested in selling mortgage loans.

Then there were several people who shared models with estimates on what was the potential loss the depositors of SVB could face if there was no backstop from FDIC and the firm had to go through bankruptcy process. One estimate highlighted the potential loss to depositors at 16.5%. The analysis done and posted on FT highlighted a potential loss of ~14%

With all the chaos that ensued on 10th, 11th, and 12th, it finally culminated in a joint statement by Treasury, Fed, FDIC before the Japanese markets were set to open and where the core message was

“approved actions enabling the FDIC to complete its resolution of Silicon Valley Bank, Santa Clara, California, in a manner that fully protects all depositors. Depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.”

With that being said, Fed created another tool in its fight to stem any fear in the markets. This was the Bank Term Funding Program(BTFP)

The Bank Term Funding Program (BTFP) was created to support American businesses and households by making additional funding available to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging any collateral eligible for purchase by the Federal Reserve Banks in open market operations (see 12 CFR 201.108(b)), such as U.S. Treasuries, U.S. agency securities, and U.S. agency mortgage-backed securities. These assets will be valued at par.

The exact collateral that the banks could use to avail the BTFP program can be found here. With the markets opening up on Monday, there was uncertainty around the collateral mentioned and whether the banks that were facing a risk to deposits had enough or even eligible collateral to assuage the fears of its customers and investors.

This uncertainty then cascaded to massive route in the stocks of small/mid sized banks with some crashing nearly 60-70% over a few days. The flight because of fright led to money flowing into the treasuries and the 2 year treasury saw 20% decline in its yields in a single day of trading.

I talked about how FDIC really aims to always find a buyer for a bank once it has been put into receivership as the quickest way to calm things down and prevent any fire sale of assets to meet deposit requests. Surprisingly, this took a while and we will probably a lot more over the ensuing months on who bid for SVB but we finally got to see 2 resolutions on SVB

HSBC UK acquired the SVB UK assets for a token £1

First Citizens BancShares is buying most of the SVB assets in U.S

At a high level, here is what the acquisition entails(from FDIC)

Today's transaction included the purchase of about $72 billion of Silicon Valley Bridge Bank, National Association's assets at a discount of $16.5 billion. Approximately $90 billion in securities and other assets will remain in the receivership for disposition by the FDIC. In addition, the FDIC received equity appreciation rights in First Citizens BancShares, Inc., Raleigh, North Carolina, common stock with a potential value of up to $500 million

The deal by First Citizens only included acquiring the SVB deposits/loans while the FDIC continues to maintain ownership of the investment securities which was at the core of the issues.

One thing that might raise eyebrows is “discount of $16.5B” for First Citizens. These type of arrangements are not uncommon and during the GFC, FDIC entered into 590 shared loss agreements. For more details, here is the page on loss sharing agreements from FDIC.

For the SVB deal, given the uncertainty in the markets and the risks that came with acquiring SVBs assets, First Citizens structured the deal with FDIC in the following way

Source - First Citizens

The exact breakdown between the assets and liabilities can be seen below. Why, if First Citizens is not acquiring the investment securities are they receiving a discount? Well, one thing we have not really talked about is the quality of the loans and what happens if the Fed keeps tightening? SVBs loans had very low loan losses but in considering that their clientele were really startups/SMBs who were coming off of a 2 year high in funding/cash availability. If the rates set by Fed stay high/continue to rise and the funding ecosystem continues to see the lows of 2022 for another year or two, what impact does that have on the broader ecosystem in terms of their ability to service the loans and continue to make payments?

This in my opinion is worth thinking about and I am sure FDIC and First Citizens probably thought about and hence agreed upon a $16.5B discount and loss sharing if it exceeds $5B

Source - First Citizens

How did Fintechs and other industry players respond?

My goal via this section is to tie it back to the SVB crisis and very much view it from the lens of the solutions being provided to people affected. Almost all the products/solutions mentioned below were something that were already available but came into limelight and saw the access democratised.

Broadly, there are 3 basic mechanisms by which you protect your funds in U.S with the most important and widely known being the FDIC insurance on accounts.

FDIC deposit insurance covers checking, savings and money market deposit accounts as well as certificates of deposit (CDs) and other similar bank products. The standard insurance amount is “$250,000 per depositor, per insured bank, for each account ownership category.” Not all bank-like products are FDIC-insured—especially those offering surprisingly high yields. FDIC insurance protects you against an insured bank failing.

The National Credit Union Share Insurance Fund (NCUSIF), managed by the NCUA, covers single accounts such as “regular shares, share drafts (similar to checking), money market accounts, and share certificates.” These credit union accounts are insured up to “$250,000 per share owner, per insured credit union, for each account ownership category.” NCUSIF protects you against an insured credit union failing.

SIPC insurance covers brokerage accounts and protects against the loss of cash and securities (excluding currencies, commodity futures contracts or warrants) at a financially troubled or failed broker. It provides protection of “$500,000, which includes a $250,000 limit for cash.” This protection seeks to restore securities and cash missing from a failed broker—not any decline in the value of those securities.

Most of the firms that were active in courting SMBs during the SVB crisis, one of the most widely highlighted products was deposit/cash sweep solution. There are several players that offer this solution but I am focussing on what I believe are the 3 biggest players.

IntraFi

IntraFi is a network and partners with nearly 3,000 of the nation’s banks and provides 2 main services that might of interest to us. IntraFi Cash Service(ICS), and CDARS(Certificate of Deposit Account Registry Service) services from IntraFi allows depositors access to millions in FDIC insurance by allowing customers to take their cash balances and sweep them into DDA(demand deposit accounts), MMDA(money market deposit accounts), and CDs. This is done through your primary account and only requires/can be maintained through a single relationship.

Benefits -

Save time without having to maintain multiple bank relationships

Earn returns on excess cash

Access funds based on your own preferences

Transparent

Below is an example of Cash sweep offering by First Republic(albeit limited to few customers as it requires you to call in and ask for it)

StoneCastle

StoneCastle helps connect depositors/investors/wealth managers access FDIC insured accounts as well. The firm provides 2 main products

Federally Insured Cash Account (FICA) - StoneCastle works with ~800 banks in providing access insured deposit accounts that are electronically linked together. Deposits in FICA are liquid, earning same day credit on purchases and providing next day liquidity on redemptions, with no investor commingling, transaction fees or redemption gates.

Institutional Cash Account(ICA) - Helps treasurers access to highly rated and money fund eligible banks via a single, convenient account. There is a minimum requirement of $20M to access this product with a clear value prop around providing same day liquidity, ability to choose banks that meet investment policy parameters, and get competitive rates on your holdings

American Deposit Management (ADM)

Closing out with ADM, they are the smallest player that provide deposit management services(upto $75M). They work with ~500 institutions and managed to help move ~$3B in deposits.

ADM offers several products for the treasury teams/institutions. See below for a high level breakdown

Having laid the foundations of what insurance offerings and sweep programs exist, we can jump into checking out how some of the major SMB focussed players did in terms of launching/modifying their existing offerings

Deposit Insurance/Sweep programs

Sweep programs have been available especially to large enterprises and SMBs for decades but with a minimum cash on hand requirement and on an ad-hoc basis. The SVB crisis led to a bit more democratisation of this feature and wide availability by leveraging the infrastructure set up via IntraFi, ADM, and StoneCastle. There are several firms that have increased their coverage/offering therefore I am focussing in highlighting a few of them.

Mercury

They offered a product called Mercury Vault which pre-SVB crisis used to offer up to $1M in FDIC insurance on the deposits. In a span of 3 days, the team at Mercury worked with their banking partners(Evolve and Choice Financial Group) and engaged in a staggered increase to FDIC insurance that they offered on the deposits. The insurance climbed from $1M to $5M where it currently stands.

Brex

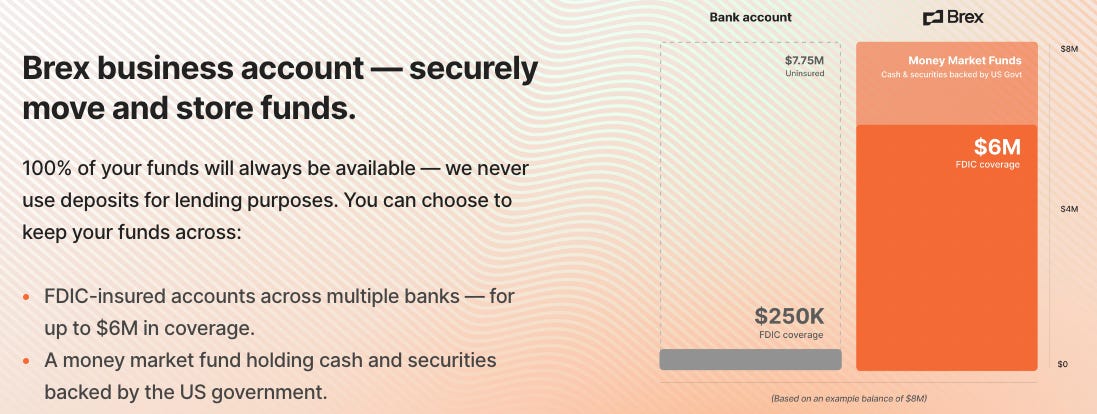

Over the span of one week, Brex ended up initiating a sweep program and increased the deposits covered by FDIC insurance to $6M.

Rho

They specifically try to target and provide services to startups that have raised atleast $1M as part of their funding rounds. Since the SVB crisis, they pushed a lot in highlighting their sweep services and protection of deposits up to $75M FDIC deposit. Rho works with American Deposit Management (ADM) as highlighted above. Enrolling in this product allow customers to access liquidity up to $3M within a day, with rest of funds available within 1 week.

AngelList

AngelList as a firm helps to bring venture funding online with private, professional fundraising tools for startups and investors. As a firm that is fairly well known within the VC/Startup community, they worked to launch AngelList Networked banking that provides sweep services and FDIC insurance coverage upto $2.75M to both VCs and Startups.

Treasury products/offering

Treasury management offerings were at the forefront of a lot of the conversations especially given cases where it was found that businesses had left millions in their checking account without having taken measures to seek protection of their funds via sweep networks, invest in treasuries etc.

Treasury management in essence tries to manage the following -

Credit and counter-party risks

Liquidity risks

Interest rate risk management

Refinancing

Exchange rate risks

Mercury

Mercury Treasury is a cash management service and provides funds via Morgan Stanley and Vanguard for businesses to invest and protect their funds. The core offering allows the customers to select the risk they are willing to accept/liquidity availability and automating fund movement via their different accounts.

Rho

Rho Treasury is a treasury management product offered to businesses to help them safeguard their excess cash by enabling them to invest in government and investment grade securities. They do specify that they want customers with >$5M in liquid assets

TreasureFi

TreasureFi primarily serves to offer businesses cash management services.

They primarily offer 4 different ways to invest your cash

Holding

This is another sweep like service that looks to partner with businesses with less than $50M in cash. The difference with this firm is that they are really focussing on providing sweep as a service

We don’t want to be your primary bank. We don’t want to disrupt your day-to-day banking needs. Instead, we want to complement your existing banking partner and provide you with the tools to easily get the most out of your idle cash

Brex

Brex offers money market-funds with nearly 95% of the fund rolling over in a day and the most recent yield being 4.21%

Jiko

Jiko is one of the few players in the Fintech space that has gone on to pursue and get a bank charter in U.S. The product that they have offered is providing businesses to map their cash flows and needs to investing in T-Bills across a timespan of 4, 13, 26, and 52-weeks.

Payment operations as a service

Modern Treasury is a payments platform that is primarily offering the service of simplifying/automating your payment operations especially as firms scale. U.S businesses are known to have relationships with various financial service providers and that inherently leads to increased complexity in managing one view of your financial health.

Modern Treasury provides 2 core products

Ledgers

Payments - Send, receive, and reconcile payments over any payment method

With SVB crisis, there was a realisation that there was a lack of clarity for a lot of businesses on their money movement capabilities, where did the money reside, and having a clear picture on the financial health by combining the views of all their financial service providers. This is where Modern Treasury has tried to come in especially with the aforementioned 2 products and tried to market themselves to the SMB community.

Financing/short term lending

The reason why I have this at the end is that this was very much a product of the weekend when the crisis was unraveling but also heart warming from the perspective of how quickly firms came to understanding how SMBs/startups stood at the precipice of not having their deposits available beyond FDIC insured and thus have potential payroll/bill payment issues.

Brex started offering line of credit for SMBs affected by funds that were locked away at SVB. The rough initial estimates from them was that they received upto $1.3B in capital requests from businesses.

Truly Financialand Ramp that focus on providing financial services to SMBs also improved upon their existing products and provide short term financing options

Post that highlighted firms that were specifically launching short term financing options for businesses impacted by SVB UK shutdown

What does the future hold?

What do I mean by this? Well no crisis such as this where the reverberations really shook financial system albeit for a short time goes without changes. These changes bring about reactions/policies that then emanate and seep its way into society, the way we work, and creation of firms whether it is because of regulatory incentives or through the opportunities/products needed by market participants.

I am going to take the liberty and accord myself some rights on making a few predictions on how things might shape up in the near to mid term. These are in no way ordered by importance, my confidence level, or probability of success.

Sweep services

Sweep services in U.S have been provided for decades and if you really went about asking your bankers about it, you could avail these services. This service really came into prominence during SVB crisis as Mercury, Brex and other fintechs worked with their banking partners to develop and launch them for startups.