As is the tradition, Mckinsey and BCG released their annual payments report in October. Instead of tackling each report separately, I have tried to weave both the reports together based on what I thought were the common themes. In putting this together, I have pulled insights from the reports as-is while adding my comments separately to bring more colour to the reports.

The post is a long one. To read in your browser, click the link below!

There is a difference of almost $500B between Mckinsey and BCG in their current estimate of payments revenue for 2021. For 2026, Mckinsey is estimating $3.3T in payments revenue vs $2.2T for BCG.

Most of the difference for 2021 and 2026 estimate between the two firm lies in how they treat Asia Pacific revenue and growth estimates.

2 things surprised me in these projections -

High growth rate expectation with EMEA. There is no breakdown of what the weights are for growth rates for Europe vs Middle East vs Africa but we do see that breakdown by BCG in their report and surprisingly Europe has a higher CAGR than MEA. More on this below.

How will the CAGR hold up given the anaemic economic growth in 2022, 2023 not looking any better as well as the inflationary pressures and wage growth that continue to persist everywhere.

Mckinsey payments report

BCG payments report

Mckinsey payments report

Comment -

Mckinsey has split its revenue by region into 2 main categories(Commercial and Consumer) and 4 sub categories.

Before going into the specifics of the data above, for those who might not know what interchange is, here is a brief explainer from Adyen website

“Every time a transaction is made via a card scheme (Visa, Mastercard, etc.), the acquirer pays the cardholder’s bank an interchange fee. The business then pays the interchange fee back as part of its card processing fees.

Payment card processing comes with three fees:

Acquirer markup: Charged by the acquirer for acquiring the funds from your shopper

Card scheme fees: Charged by the card scheme for using its network

Interchange fee: Charged by the cardholder’s bank

Interchange fees make up the most significant chunk of card processing fees.”

Credit cards -

LatAm and NorthAm stand out for the share of credit card fees/interchange as % of consumer revenues. These two regions are known to broadly have the highest Interchange rates. Europe proceeded to enforce regulation and cap debit/credit interchange significantly in 2015. Australia similarly put a cap on IC in 2017.

Below is the closest I have come to seeing credit interchange across countries courtesy of Kansas City Fed. The data is a bit dated and would appreciate getting linked to anyone having a better view on this but for now I suppose this suffices.

Credit and Debit Card Interchange Fees in Various Countries - Kansas City Fed

Account related liquidity -

Anyone interested in getting a country level breakdown for NIM(pre-pandemic data) aggregated together can use this link

Over the pandemic we saw suppression of the NIM given excess liquidity in the system via quantitative easing and excess savings from consumers. With rates rising across the board, albeit at a slowing pace now but at the same time having a reduced demand from consumers for lending/economic doldrums, it would be really interesting to see what the impact of that is on NIM for banks especially over the next 2 years.

Domestic transactions -

EMEA region stands out for both commercial and personal categories for % of revenues that come from this category. The underlying reason ties to the above two categories that I talked about. With interchange rates that are capped, NIM margin being compressed due to negative rates or 0% rates set by ECB over many years, financial institutions predominantly focussed on adding fees on banking services that they provided to customers. This became the core source of revenue.

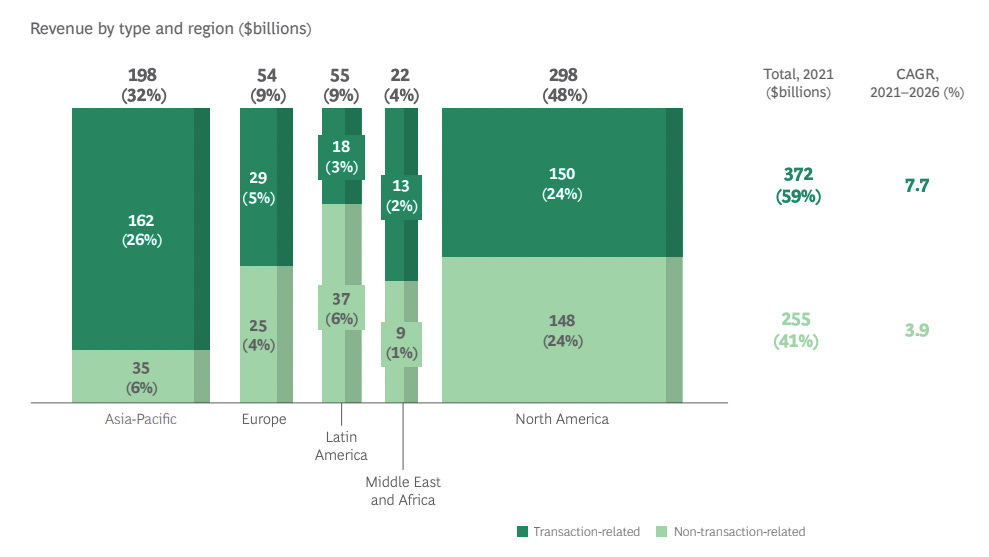

BCG payments report

Comment -

Unlike Mckinsey’s regional breakdown, BCG grouped the revenue breakdown by transaction vs non-transaction. According to the report, here is the breakdown of the two categories -

Transaction-related (primary) revenues —> transactions made with cards and non-card instruments.

Non-transaction related (secondary) revenues —> revenues from deposit interest, card maintenance, account maintenance, revolving revenues from credit cards, foreign exchange, value-added services, and overdrafts.

Over the past decade or so, we have seen numerous countries move towards launching RTGS(Real time gross settlement) systems and broadly limiting interchange rates. With rising rates and what becomes of net interest margin, I would be surprised at transaction related primary revenues continue to grow their share of the total revenue pie. Two possibilities on why BCG believes the share to not fall. One could be around the massive B2B payments(for example - 5.3 billion B2B payments—valued at $50 trillion over ACH in U.S) migrating away from how it is now over to A2A or cards especially in certain regions. Second is the ever diminishing usage of cash and migration of those transactions to existing payment methods.

Mckinsey payments report

What are the major forces that are reshaping the landscape?

First, the pandemic accelerated the shift from cash to contactless digital payments that was already under way among consumers. Digital payments continue to increase Globally, between 2018 and 2021, the number of noncash retail payment transactions have increased at a compound annual growth rate of 13 percent; while in emerging markets, that figure is 25 percent. Some of the fastest growth occurred in emerging markets in Africa (Morocco, Nigeria, and South Africa) and Asia

Comment -

FIS had a fantastic breakdown in their payments report around e-com and POS payment methods for every region. MEA region is forecasted to see the largest drop in cash usage by 2025.

FIS payments report

An example of a country that has seen significant reduction in cash usage over the past decade is Sweden. There are all the usual suspects(covid, penetration of cards, ease of use of other methods, risk etc) as to why cash usage is reducing but one notable mention for Sweden has been the usage of their P2P system called Swish

There is a whole section below on wallets and what a feature journey could look like. Swish now claims to have roughly 8 million customers, facilitates not only P2P transactions but also between merchants and consumers. We are seeing the same patterns across the globe not only with P2P/digital wallets but also payment systems such as UPI in India, PIX in Brazil and Instapay in Philippines.

Another critical element in less usage of cash is governments preferring people to spend via other payment methods. Some reasons around this preference revolves around plugging tax leakages, distribute aid to people who need it in a cost effective and timely manner, and facilitating interoperability.

Second, e-commerce continued to grow and evolve, with global volumes increasing by 25 percent between 2019 and 2020 and expected to grow by 12 to 15 percent a year to 2025. A main driver of the past high valuations of fintechs and attackers was the expectation of revenue growth through expanding customer relationships. This opportunity persists as payments increasingly serve an integrated, value-added commerce role rather than merely executing a stand-alone financial or money movement transaction. The most common current embodiment of this trend is commerce facilitation, extending beyond checkout and payment to enhance the commerce journey.

Macroeconomic environment - inflation, interest rates. Factors like the global energy and commodities environment have led to growth uncertainties and increase the likelihood of recession, differing by region. This, in turn, will have impact on the liquidity and investment strategies of many companies and households, altering payments economics on both the demand and supply sides.

Inflation, in contrast, will create an organic uplift for the transactional components of payments revenue priced as a percentage of value, such as credit card interchange. Fixed transaction-based fee components might remain unchanged, potentially creating a drag on profits as related costs are rising under influence of the same inflation.

Comment -

If we consider the broad categories that Mckinsey classified the payment revenues by, I would consider cross border payments and credit cards as broadly being inflation proof. Account related liquidity which broadly encompassed Net interest income + overdrafts and Account maintenance fees are not necessarily scaling with the inflation.

How long we continue to have low growth, how that extends to job gains/losses and does wage growth cover for the price increases consumers are seeing will start flowing into the credit card data. Considering U.S.A which is the biggest credit card market, right now all the major banks are highlighting no major shifts in delinquencies and are seeing consumers still have a healthy cash balance in their account. If the situation takes a situation for the worse, then the revenue growth will quickly cascade into negative territory and lead to banks having to book reserves for loan loss reserves.

Account related liquidity especially NIM will most likely see an uptick over the coming quarters. In my opinion, there are 3 things that I believe will lead to the banks not really seeing a material positive impact of rising rates.

One of the biggest lending sources for banks is mortgages. Rising rates especially in U.S and U.K has been leading to significant drop off in demand for these mortgages. This very much looks like what happened in 2020 during the covid crisis where banks were flush with cash from the government payouts to its citizens but had muted demand for loans thus creating a massive pressure on their NIM.

In addition, with rising rates, you are going to see banks having to increase the savings rate they offer to consumers.

Finally, there is massive competitive pressure from Fintechs who have already started increasing and finding ways to give customers a decent interest rate on their savings. This might start enticing consumers to move their cash easily to these accounts and create pressure on the banks to spend more on retaining these customers, offering incentives on other products, or raising their rates.

Geopolitical environment - More countries are moving to greater payments regionalisation and localisation. A by-product of the focus on regional and national payments infrastructures will be the increased complexity of regulations across markets. Fragmentation and the need to localise will likely create continued disconnections across compliance and security requirements, despite ongoing international dialogue to standardise. This creates opportunities for payments providers that can simplify cross-border payments for customers or create turnkey solutions for related services—say, know your customer (KYC) as a service, digital ID, and security. Geopolitical events and sanctions have also had an impact on trade and treasury international payments, strengthening regional bonds and creating shifts in segments and geo-corridors.

Barring Africa, the past decade has seen Government/Central Banks plan or actually launch instant payment systems. There is an aspect of proliferation of smartphones and 4G/5G that allows billions of people to be connected. Mckinsey highlighted that “Instant-payments volumes are increasing 40 to 60 percent globally” and this growth is also visible in countries such as UK/mainland Europe where there has been a broad adoption of such payment systems.

Taking Stripe, Adyen, and Paypal as examples, these 3 payment processors have been chipping away at this very problem by pushing themselves towards having a global first attitude and weaving together the inherent complexities of each country and the varied payment systems. Stripe as of right now is available in 47 countries whereas Adyen in around 40.

For those that have not been keeping track, 2023 will see the launch of FedNow service. U.S has real time payment systems but this is the first push by Federal Reserve in providing a service accessible to all the depositary institutions in U.S.

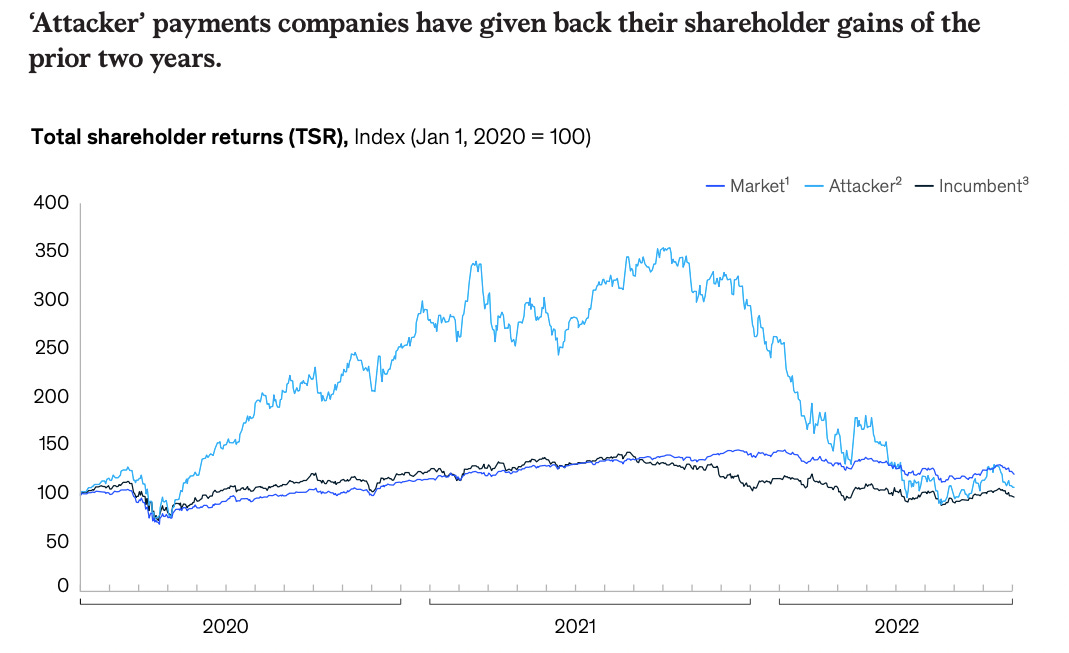

Capital markets reset. While “attacker” payments companies significantly outperformed both the broader market and “incumbent” payments players over the last few years in the capital markets, 2022 saw a significant reset in valuations. This valuation reset creates opportunities across the landscape as incumbent companies consider acquisitions and attackers focus on sustainable growth and a path to profitability.

BCG payments report

Mckinsey payments reports

BCG payments report

This decrease in many payments companies’ valuations could provide a catalyst

For consolidation by incumbent payments companies and tech company entrants, given the lower multiples and reduced feasibility of IPOs as an exit strategy for private firms.

Attackers might, in turn, shift their strategic approach, moving from “growth at all costs” to a fundamentals-focused and cost conscious operating model with renewed focus on profitable customer and account growth, cash flow, and operating performance.

These companies will likely revisit monetisation opportunities—for example, partnerships with incumbent payments companies and companies in other sectors— while maximising the efficiency of their existing operating models. When the going gets tough, adept unicorns can quickly pivot into workhorse roles.

Comment -

FT Partners deal activity

FT Partners in its latest release highlighted the above deal flow activity. Comes of no surprise that after the bumper year of 2021, we are seeing muted volume whether it is financings or M&A.

Klarna(BNPL firm) has probably seen one of the largest declines in its valuation(85% in its last fundraising round). Stripe took a haircut on its valuation and Adyen that has been in expansion mode especially in their hiring plans has seen its stock price fall by roughly 40%.

Technology modernisation - For instance, banks are aggressively modernising their core systems to real-time, third-generation cores and updating their payments infrastructures, largely in response to the continued rise of instant payments, open banking requirements, and cloud technology.

The share of IT spending by banks on legacy infrastructure is expected to decrease from roughly 50 percent in 2021 to about 10 percent in 2024, thanks to private cloud and true multi-cloud solutions. This step change in infrastructure modernisation is a result of increasing pressure to support the transition to instant, open, integrated, and cloud-based solutions to meet continuously rising customer experience expectations across the commerce journey.

The need for digital investments keeps growing. In addition to dealing with mounting competitive pressures, banks must evolve their processes to address a number of sweeping mandatory market standards and regulatory changes. Few examples of investments that need to be made -

By the end of 2022, banks must comply with ISO 20022 to implement MX formats (XML message definition) for cross-border payments, with an interim period until 2025 during which use of the old SWIFT MT formats will still be permitted.

By 2023, European banks need to implement updates mandated by the Single European Payments Area (SEPA) rule book, including upgraded MX formats for SEPA payments. In parallel, many banks are working on additional payment use-cases—such as request-to-pay solutions, a messaging functionality that initiates an instant credit transfer.

Similarly, to comply with open-banking rules, institutions must find ways to transform legacy IT for payments into modular, cloud-based architectures that can support creating and sharing APIs. Transaction banks will also need to prepare their systems to handle digital currencies, especially as more central banks around the world launch pilots for CBDCs.

Comment -

Earlier in the year, we saw JP Morgan in its earning call talk about increasing their tech spend by almost 30% compared to the previous year. Core part of this spend has been in modernising its tech stack and we can see this in how they have approached their entry into the UK market. The firm has partnered with Thought Machine to overhaul its core banking operations. In UK, JPM entered the market with and offering that has been digital first, has seen the firm acquire and integrate Nutmeg as part of its offering, and seen the operations grow to having almost a million customers and roughly £10B in deposits.

The value of this integrated experience for customers helps explain why embedded finance reached $20 billion in revenues in the United States alone in 2021, according to McKinsey’s market sizing model. According to our estimates, the market could double in size within the next three to five years.

What makes the next generation of embedded finance so powerful is the integration of financial products into digital interfaces that users interact with daily.

Mckinsey payments report

Mckinsey payments report

Who is capturing the value? Not all players benefit equally from the rise of embedded finance. As in banking in general, revenue primarily accrues to risk takers and to the distributors that own the customer relationship. The majority of revenues from embedded-finance lending products (55 percent of $14 billion in the United States in 2021) accrued to the balance sheet provider—the firm bearing the risk of credit default. However, where payments and deposit products were concerned, the distributors who owned the end-customer relationship benefited most. In lending, for instance, they earned $4 billion of the remaining $6 billion revenue pool, equal to 30 percent of total revenues.

Comment -

11:FS did a report on Banking as a Service and had the below as an example of the different players involved and the problem areas that they tackle. Mercury is an SMB Neobank. Pricing for the license holder or the BaaS provider is based on the number of api calls/transactions that happen. Mercury here gets to focus on the core customer experience, solving problems, finding where it fits on the competitive landscape and use all that to determine its pricing advantage and gain most of the upside in this transaction lifecycle.

11:FS - Banking as a Service report

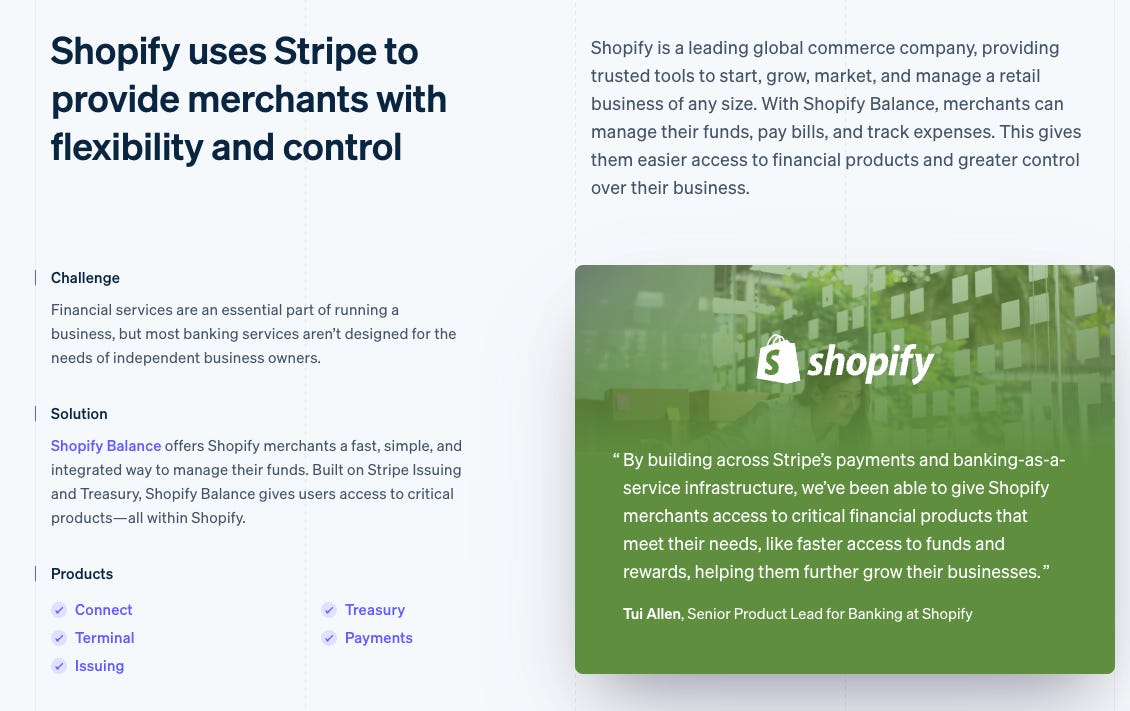

Shopify is another example that has understood the importance of providing financial services to the merchants that use its platform. They have partnered with Stripe and also have ownership stake in the firm. In its latest quarterly report Shopify highlighted that “Gross Payments Volume ("GPV") grew to $25.0 billion, representing 54% of GMV”. These are payments that are processed via Shopify payments and is powered by Stripe(believe they are the only one powering them). Not going too deep in the weeds of country/pricing breakdown but assuming a conservative 2% per transaction, that would imply $500M in revenue for Stripe.

Product depth. A few technology and balance sheet providers are building deep expertise in specific embedded-finance categories such as issuing, in order to claim outsize market share in these niches. They develop innovative use cases—such as just-in-time fund deposits into cards or crypto-linked payment authorisation— as a basis for creating novel financial products for end customers.

Program management support. Many distributors that are new to embedded finance are understandably concerned about how to build, sell, and service a financial product for end customers. Some of them may see the regulatory and reputational risk attached to financial products, especially lending, as an insurmountable hurdle. To help them overcome the risk, many embedded-finance technology providers are offering sales, servicing, and risk management expertise or are orchestrating other partners providing them.

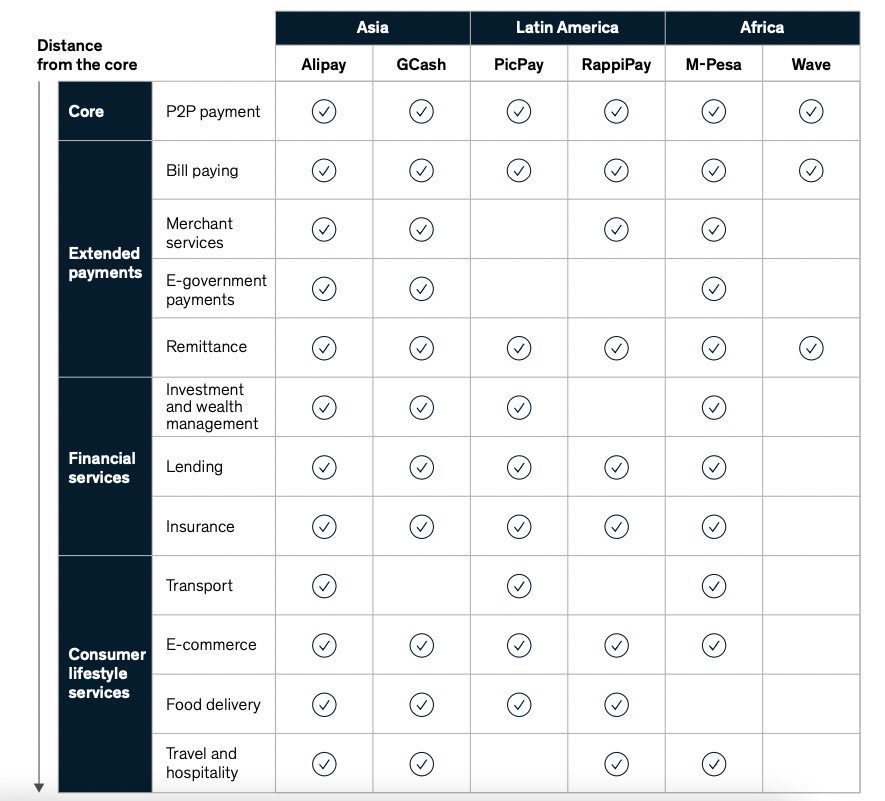

Wallets are the leading e-commerce payment method in the Philippines (accounting for 31 percent of transaction value), Vietnam (25 percent), and Indonesia (39 percent), and they take second place in Thailand after bank transfers. Some wallets have achieved very high penetration levels in these markets. In the Philippines, for example, the registered users of the top two wallets, GCash and Maya, account for 83 and 65 percent of adults, respectively.

Wallets are more embedded in customers’ daily lives when they are part of ecosystems. This enables them to grow by extending into e-commerce, ride hailing, food delivery, messaging, travel, and other adjacent categories. For instance, prominent ride-hailing players in Southeast Asia, such as Grab and Gojek, are looking to capitalise on their high-frequency use and rich customer data by extending into groceries and other categories with larger ticket sizes. Players with higher ticket sizes but lower frequency of use, including e-commerce platforms Jumia in Africa and Shopee in Southeast Asia, are pushing in the opposite direction, seeking to boost user engagement through gamification and other approaches.

Mckinsey payments report

Comment -

Mark Goldberg in his writeup on Cash app had the following product launch image(courtesy FT Partners) over the years. If we follow the roadmap, Square followed the quintessential journey in having P2P payments to then going down vertically and building countless features as we can see in the roadmap below.

Cash app has also recently started allowing its users to send money to people in UK and I suppose it will be the horizontal push across different regions that will be the interesting gameplay here for Square. In acquiring AfterPay, they also have the ability to leverage that firms presence across 13 countries and potentially use that for Cash app market expansion.

Mckinsey payments report

Merchant Acquirers and Issuers

Merchant acquiring industry is maturing rapidly, as the COVID-19 pandemic may have created permanent shifts in the market from offline to online. Many competitive challengers are now at scale and expanding into new regions, segments, and products.

From 2021 to 2026, our analysis suggests, revenues for the acquiring industry will expand at a CAGR of 8.7%, raising its total revenue pool to $160 billion. Revenue pools from SME merchant acquiring will grow at a faster rate than those from larger merchants, contributing roughly 75% of incremental revenue expansion

BCG payments report

Several trends evolving in the merchant acquiring field

The competitive landscape is shifting - Most challengers evolved from serving a niche segment of merchants to offering a wide array of payments, banking, and value-added services to a broader range of companies. We are seeing multiple playbooks, one of which is to leverage a two-sided network and offer compelling value to both merchants and consumers.

Comment -

The 3 largest merchant acquirers in U.S are -

J.P. Morgan Payments

FIS

Fiserv

JP Morgan and the products it offers is something most people are fairly familiar with. Building a two sided network might not be the strategic focus at JPM but whether it is in being an issuer and a merchant acquirer, providing banking services to millions of customers and SMBs as well as large corporations, it really does showcase what a strong position they find themselves to be in.

Looking at FIS, below is the suite of products that they offer

The product suite is broad but the firm has a B2B focus. It primarily known for its role as a merchant acquirer and has grown massively by positioning itself in that market and through acquisitions(Worldpay being its largest).

ISVs are gaining more power and influence with SMEs - In key acquiring markets such as the US and Europe, more than half of all small to midsize merchants now use ISVs. In these markets, ISVs now command almost 30% of merchant-acquiring revenue pools, a share that is likely to grow rapidly over the next five years. The platforms that these software companies provide—many tailored to specific industry verticals such as Toast for restaurants, Mindbody for Fitness, and Jobber for field services—have made it easier and faster for entrepreneurs to open an online business while bypassing traditional banks and payments intermediaries

Comment -

Last year, Tanay Jaipuria probably had the best breakdown of Toast S-1. Two things stood out for me in the post.

The concept of SaaS 3.0 where in addition to providing bare minimum services that ISVs have in the past, providers are extending their product suite and embedding more financial products.

Evolution of SaaS companies via Stripe

Toast Capital - Toast defines it as “Toast Capital connects restaurants in our community with access to funding to meet their needs and fuel their growth – without any compounding interest or personal guarantees.” This is very much in line with what is called revenue based financing. Several firms in this space(Pipe, Capchase, ClearCo etc) have grown massively over the past 2-3 years.

Utilising revenue/cash flow of the restaurants for lending decisions probably provides far better view into the capability of the business to pay back the loan compared to relying solely on some combination of traditional lending which is credit scores + relationships.

Large merchants see payments as a critical element of the customer experience. - As the availability and reach of e-commerce grow, customers find that they have more purchasing options at their disposal and fewer barriers to switching. With buyer loyalty less assured and margins tighter, merchants globally are optimising for three objectives: creating a seamless, frictionless payments experience; driving incremental revenues through their existing payments offerings (such as through co-branded relationships); and achieving greater cost efficiencies.

Embedded finance could generate massive value for players. - Our research indicates that a significant number of SMEs are eager to obtain everything from working capital finance to business credit cards

A Blueprint for Growth

Define winning plays. - Traditional acquirers must identify which opportunities are most feasible, given their current resources and positioning, and which can deliver the greatest potential returns. Rather than spreading themselves too thin, acquirers should study the composition of their existing customer base and prioritise industries in which they can differentiate and win. SMEs bring the prospect of higher take rates (often ten times greater than those for large merchants) and lucrative embedded-finance revenues. But the cost of acquiring such accounts is relatively high and requires seamless onboarding. Conversely, large merchants have much lower take rates but offer significantly higher volumes and the opportunity to cross-sell into adjacent revenue pools such as authorisation solutions and return-and-dispute management.

Comment -

Payment processors such as Stripe, Paypal, Square etc have been fairly clear on targeting SMBs and having them as their primary focus over the years. Stripe has been moving upstream towards targeting large enterprises which to a large extent remains in the domain of Adyen and other established players.

Become a trusted advisor to large merchants. - Acquirers have an opportunity to become a partner of choice for large merchants. Indeed, many such merchants need help assessing and enabling the BNPL opportunity, managing their commercial journeys, and determining which payment methods are most suitable in different markets from both a customer perspective and a cost perspective

For merchants interested in setting up or expanding a digital marketplace, acquirers can provide key services such as pay-in and pay-out, sub-merchant management, and accounts payable/accounts receivable automation. Acquirers can also establish internal environments to support innovation in payments—for example, by allowing large merchants to test new commercial journeys and optimising tradeoffs through analytics and artificial intelligence. Such efforts can lead to a more trusted relationship between the acquirer and the merchant.

Comment -

Adyen is known for primarily working with and having large enterprises as its clients. A quick look at Adyen’s website leads us to this

If you consider Uber as an example, given its global presence, what becomes of utmost importance for the firm is to ensure that the authorisation rates for the payment method that the customer selects are high and is a smooth experience. At the same time payouts to drivers all across the world in the local currency is as important a use case for them. This is where Adyen comes into play. Ensuring optimal routing, smoothing out the experience, managing fraud but still keeping authorisation rates high, managing cross border flows, and working with Uber on new use cases.

Improve revenue management. - Acquirers proactively adapt their merchant offerings to the macroeconomic environment, enabling new solutions such as faster settlements and easier access to working capital, which in turn can help merchants mitigate cash-flow issues. Acquirers will also need to adopt a more active revenue-management posture to improve back-book and front-book pricing. Starting with price setting, acquirers should optimise for higher-margin structures where possible and consider steps such as tiered pricing

Take proactive risk and compliance management actions to create resilience. - With the possibility of a recession looming and with increasing regulatory scrutiny in the payments space, incumbent acquirers must prepare for greater volatility and shore up their risk-and-compliance management practices. As a first step, they should define their appetite for risk, which entails conducting a review at the overall portfolio level and per industry. Next, they should develop a toolkit to reduce exposure to potential loss, part of which will involve defining requirements for merchants. Further, acquirers can harmonise onboarding guidelines and processes both to ensure efficiency and to mitigate compliance risks stemming from shifting regulation. They must consider credit-risk factors for merchants, along with all related scoring, while establishing contract terms for new merchants

How Issuers can build advantage

The issuing industry has maintained steady growth in recent years. Looking ahead, we expect issuer revenues, which amounted to $627 billion in 2021, to keep rising at a healthy 6.2% rate annually over the next five years. Primary (transaction-related) revenues, mainly from interchange fees, will drive much of this growth (CAGR of 8.4%), followed by secondary (non-transaction related) revenues that include foreign-exchange and annual card fees (CAGR of 3.9%). (See Exhibit 5.) We further expect issuer revenues to reach a value of over $1 trillion globally by 2031.

BCG payments report

In particular, two major shifts are reshaping the issuing space.

New payment methods such as BNPL have opened the door for payments players to move beyond a transactional role

Comment - I don’t consider BNPL firms as being a replacement for debit/credit cards but if anything these firms have definitely found a fit with Millennials and Gen Z. There are several questions around how much of it had to do with lax lending rules, excess cash circulating in the economy etc and how we are seeing it play out now with massive haircuts in the valuation that we have seen with Klarna and the public BNPL firms in the Australian stock market.

What is undeniable that the BNPL firms have learnt to use the transaction data in a much smarter way. Alex Rampell talked about this in detail. I also did a deep dive on the BNPL industry and trends last year and don’t necessarily believe much has changed since then.

Consumers expect richer rewards and a more personalised loyalty experience - the pandemic has spurred a revolution in the traditional value and perception of rewards, while the growth of digital wallets has made cards less visible in daily purchases. With travel curtailed, traditional mileage, restaurant, and entertainment rewards have had less allure for consumers, forcing issuers to experiment with new offers such as expanding cash-back or statement credits to new spending categories (such as food delivery and streaming services) or extending “pay with points” to all types of spending. Such changes have added spark to rewards portfolios, but at a price: issuers in the US, for example, are seeing the costs of their loyalty programs rise by an average of 5 percentage points higher than the corresponding growth in customer card spending.

Comment -

Covid had a significant change that card issuers/players had to re-think their card reward programs. What did come of it were some interesting ideas on how to improve reward programs beyond what is mentioned here -

Making it easy for customers to redeem their points by reducing redemption price.

Enticing customers with varied rewards depending on type of spend.

Keeping customers engaged by enrolling different reward partners on a quarterly basis.

Tying rewards that cards offer in a way to potentially incentivise customers towards other products that the financial institution might be selling.

In tying all of the above, firms should be leveraging analytics to understand what % share of the wallet are they capturing in running these reward programs. Another critical aspect of these programs is to also try and understand segmentation within your customer base. From a marketing perspective, identifying these segments by how these customers behave and figuring out how to retain these customers vs trying to spend your way to gaining new customers who might not be sticky could be the differentiator between having and not having a successful rewards program.

Moves That Issuers Should Make Now -

Diversify revenue streams by turning data into a superpower. First-party data is becoming increasingly valuable, and issuers sit on troves of it. As third-party cookies are phased out, marketers are finding it harder to obtain high-quality consumer data efficiently. By leaning on their rich data assets and sharing them in an anonymised, regulation-compliant manner, issuers can enhance the value of the data that they provide to merchants and can open significant new revenue streams for their own businesses

Become a trusted third-party data source. Issuers that also have a merchant acquiring arm could create an entirely new business model by providing merchants and other partners with high-quality anonymised consumer data to support their own personalisation initiatives. In addition to providing sanitised raw data, issuers should invest in strong analytics capabilities that merchants can leverage to better understand customer behaviours and unlock cross-selling opportunities.

Buy now, while valuations are attractive, to modernise the approach to data. Issuers will need to significantly alter their approach to monetising data. In addition to revisiting their data architecture, governance, tech setup, existing partnerships, and go-to-market methods, issuers could leap ahead on this journey through inorganic moves. With market volatility limiting digital players’ valuations and access to funding, now may be a smart time for issuers to acquire distinctive technology. Fintechs—especially in the BNPL, data aggregation, and loyalty spaces—could bring critical data-management and technological expertise to help issuers create the data-driven ecosystems they will need to support merchant-funded offers. Issuers could also leverage best-in-class go-to-market capabilities to optimise affiliate marketing budgets and investment returns for merchants.

Protect the core business from a potential downturn. Issuers should ensure that they are prepared to weather a possible economic downturn and to shore up their underwriting, collections, and recoveries capabilities. Priorities should include the following actions:

• Adopt an integrated multichannel strategy. Deliver unified campaigns to manage collections across several platforms while prioritising SMS, email, and push notifications over the phone—all while complying with regional outbound call regulations. Recovery rates will likely increase, and reputational risk will diminish.

• Empower customers. Develop an autonomous digital first collections model to provide customers with self-servicing options. This initiative will aid, in particular, customers that are prone to missing monthly payments.

• Strengthen the organisation. Empower risk and collections teams with higher self-governance levels, rapid testing capabilities, and advanced analytic techniques.

Payments players today face a strong case for strengthening their risk and compliance activities in order to continue on their growth paths and install required safeguards for their businesses. Market participants must address four key risk dimensions in the coming years:

Financial Risk. Managing financial risks (for example, in merchant acquiring or card issuing) requires keen vigilance in a turbulent macroeconomic climate. A holistic financial-risk operating model not only provides downside protection from heavy losses, but also serves as a steppingstone to conducting business in attractive high-risk segments.

Compliance Risk. Owing to rising regulatory scrutiny, reputational risk, and the prospect of a macroeconomic contraction, compliance risk in payments demands urgent attention. Payments providers should ensure that they have a robust compliance operating model in place to strengthen know-your-customer and transaction monitoring. Areas of attention include compliance strategy, governance and people strategy, compliance risk management, and top-down compliance culture

Cyber Risk. Online payments are a prime target for fraudsters, and fraud shows no signs of abating. Indeed, card and electronic payments represented 84% of the £730.4 million ($832.7 million) lost to fraud in the UK

Crypto Risk. As the cryptocurrency and decentralised finance industry has matured, and as various speculative bets have expanded, demand for regional and global crypto regulations and internal crypto-risk management has increased sharply. Some countries are banning private cryptocurrencies in order to push their own CBDCs; others are promoting countrywide and government supported stablecoins as payment alternatives, while awaiting the development of CBDCs.

What can the Incumbents(Networks and Banks) do to sustain their business, grow and build resilience?

Our analysis suggests that networks’ revenues—from both international and domestic schemes combined—will rise at a CAGR of 8.9% from 2021 ($63.8 billion) to 2026 ($97.9 billion). The major challenge is that more countries are seeking to exert greater control over their domestic payments infrastructures and limit the role of international card networks in them.

Local data storage rules, compliance/regulation, prevalence and proliferation of local payment systems, and geo-political tensions all seem to be major risks for the network operators. These risks have always existed but if anything, the past few years has shown a heightened risk around these factors.

I believe that Mckinsey/BCG are optimistic in the network players being able to deal with this and continue with the trend of taking a larger share of the wallet via elimination/reduction of cash usage, permanent change in behaviour post covid, and continue to provide businesses incentives and tools to switch their B2B spend/payments that span in trillions.

To go beyond inertial growth and protect against downside risks, networks must diversify and take a number of actions.

Go vertical - Developing vertical-specific product propositions in industries such as gaming, construction, health care, and transportation can help networks acquire a foothold in high-growth sectors. Prior investments in areas such as push-payment solutions (in which payments are credited to a user’s account), A2A payments, and payments acceptance technologies such as SoftPOS for small businesses. Networks should set up their sales forces and partner with acquirers and fintechs to create market-tailored solution bundles for software-as-a-service (SaaS) companies in fast-growing industry verticals.

Comment - I could be wrong about this but I feel that network players such as Visa/Mastercard etc are better served in working directly with the issuers/acquirers/payment processors in formulating solutions for a specific industry. Mastercard does have several case studies on how it has worked with specific industry players but a lot of it revolves around in helping the client understand its customer better.

In line with what I said, I did find Visa and its focus on Issuers/Fintechs/BNPL players etc via its different partner programs.

Accelerate the adoption of open banking and A2A payment flows - Some networks, through their acquisition of open-banking connectivity players (such as Visa’s purchase of Tink and Mastercard’s purchase of Finicity), are preparing to play a larger role in establishing a new network pertaining to data flows. The short-term opportunity for networks lies in cross-selling open-banking solutions to their issuer customers or selling card solutions to open banking connectivity users. Networks can also help open banking participants manage their payments compliance activities, taking a costly requirement off their shoulders, especially in the case of cross-border A2A payments. Networks are increasingly well positioned to develop differentiated application programming interface (API) pricing solutions to support open-banking data use cases in areas such as lending decisions, loyalty, personal finance, wealth management, accounting, fraud detection, personal real estate, and personal insurance. Networks can build VAS to remove frictions for open-banking ecosystem participants in such spaces as consent management, dispute management, and risk management.

Comment - In what is fortuitous timing, I happened to read the transcript of Ryan McInerney(also incoming Visa CEO) at the Global Fintech conference and this is what he had to say about Open Banking

Gain first-mover advantage in new growth frontiers - Although card payments remain poised for growth, the rise of alternative payments instruments and rails could fragment the landscape, posing a risk to the networks as payments volumes spread across fiat and digital currencies. B2B payment flows represent the next growth frontier for networks. Along with person-to-person, business-to-consumer, and government-to-consumer payments via emerging channels such as push-to-card, B2B represents a potential $185 trillion opportunity per year globally, as estimated by Visa. Some large networks are investing in B2B solutions and platforms, but they have not had much success in penetrating that new payment flow opportunity. Moreover, they have yet to develop the use cases, technology, and process integrations they will need to fulfil the often-complex requirements of those flows across multiple stakeholders, instruments, currencies, and geographies.

Comment -

Visa over the years has made several acquisitions but two stand out in relation to cross border capabilities. First being Earthport and second being that of CurrencyCloud.

We talked extensively at the beginning about the ever growing need of cross border payments and how a key differentiating factor could be in firms leveraging their licenses across the globe, understanding of KYC/compliance across several countries and integration disparate payment systems + new payment systems that are on the rise.

When we consider Visa(other players exists as well but considering Visa for the sake of this point), I truly believe that they find themselves in a strong position of leveraging their brand recognition and capabilities to gain an increasing share of the wallet. Now, I mentioned the two acquisitions they made before. CurrencyCloud plays in a field with many players where they embed with other financial players and provide cross border capabilities to them. I unfortunately don’t have the details on how extensively they have been integrated within Visa but given the B2B nature of the two companies, this could potentially become an extension of Visa’s strategy into cross border payments.

Banks that meet the evolving needs of CFOs and treasurers could tap into a global revenue pool worth up to $494 billion in 2021, a sum that our forecasts suggest could grow by a CAGR of about 9.2% through 2026 to $768 billion.

BCG payments report

Key challenges -

Corporate customers have heightened expectations. With liquidity concerns paramount, CFOs and treasurers need full transparency with regard to their companies’ incoming and outgoing cash flows. They also need predictive intelligence to manage and schedule their domestic and cross-border payments, and they need it delivered over a convenient and secure corporate-to-bank interface. Also, CFOs and treasurers need help with back-office digitisation and data reconciliation. Many would like to integrate transaction data across their myriad banking relationships, legal entities, and operating jurisdictions and then transfer this information into their corporate systems—such as procurement, accounting, and enterprise resource planning (ERP)—on an automated, near-real-time basis

Non-banks are posing a greater competitive challenge. Banks used to be the primary provider of transaction banking services, but not anymore. Both the number and the variety of entities competing in corporate payments, cash-flow optimisation, and financing have grown massively in recent years. Today, banks face challengers in each segment of the wholesale transaction banking landscape, forcing them to defend share across the value chain.

Comment -

One of the most well known picture is disintermediation of Wells Fargo products and the Fintechs that are targeting that specific area.

CBInsights

I am a bit conflicted on this and obviously with the benefit of hindsight, it seemed bold to believe that disruption of traditional banking players was a guarantee. I am always reminded of the seminal post by Alex Rampell almost 7 years ago where he said the following - “The battle between every startup and incumbent comes down to whether the startup gets distribution before the incumbent gets innovation.”

Banks have 2 advantages that stand out - 1. They are the medium through which Central Banks are able to run monetary policy and in most of the countries this is a very critical feature of the system. 2. To be able to do so, they have very much surrendered to rigorous compliance process. What have the banks gotten in place of this? Regulatory licenses that help differentiate them from non bank financial institutions and restrict lending activities to such firms.

I don’t mean to turn this into a banking primer but these advantages are probably here to stay. Well run banks flush with profits are starting to understand the competitive threats posed by fintechs and investing heavily in their tech operations, products they offer to customers and are finally finding that innovative streak to catch up to the competition.

Winning Moves That Wholesale Transaction Banks Should Make Now

Think like a platform player. Value is flowing toward integrated journeys and ecosystems. Banks need to embrace this shift and scan the market for opportunities to create smart platform plays. Goldman Sachs, for instance, created a BaaS platform that allows corporations, fintechs, and e-commerce marketplaces to access a full suite of treasury services

Comment -

Banks have always provided numerous products and functionality especially to large enterprises. The international presence for banks such as JP Morgan, Citi, HSBC etc has been the strategic key in helping them work with Fortune 500 companies providing banking, custody, treasury and other services.

Therefore, I am missing the point here. Can banks do better in integrating their services together to provide seamless services? Sure. What is more critical is for banks to really determine what is their strategic focus. Who or what kind of business do they want to focus on? Do they want to continue having a global presence and deal with the compliance and regulatory cost associated with it? Where do SMBs fit into their strategy?

One of my learnings around strategic decision making is not only determining what to do but being very clear on what not to do.

Leverage transaction banking data to support SMEs and open new revenue streams. Transaction banking activities generate a large data trail. Managed appropriately (and with customer data privacy a priority), these data assets enable banks to provide customers with

Tailored working-capital analytics

Real-time liquidity modelling tools

Balance-sheet insights

Spending, expense, and invoice management

Customisable mini-ERP offerings

Software enabled dashboards that make it easy for business owners to view their incoming and outgoing payments.

Tying to the above point, Kearney did a series on open banking and put together a rough sketch on what a dashboard for an SME could look like. SMEs do have access to accounting softwares Xero, SAGE, SAP etc that provide real time financial view/health so that might not be something where the value add exists. On the contrary, bringing together data from across different systems, understanding and providing insights on how working capital can be efficiently managed, and providing bridge loans/other forms of funding to smoothen out cash flow is solving for a fairly common problem.

Another area of focus which has been the major focus for Fintechs all across the globe is “Spending, expense, and invoice management”.

Lorenzo Chiavarini did a write up on the spend management scene and we are starting to see Fintechs/SME neobanks understand the importance of this problem.

Dealroom

One notable company on which much has been written is Ramp(Packy McCormick has one of the best writeups). Ramp started with a focus on U.S businesses and the core product was expense management + corporate cards. My belief is that over time they have understood that to be their wedge product and entry point to their core SME target but at the same time their product roadmap shows how they are building upon the pillars of business needs mentioned in the main point above.

2020 Ramp roadmap and release

2021 Ramp roadmap and release

Build a modern, modular payments architecture. Given the trend toward integrated, platform-based services, wholesale transaction banks must modernise their IT architectures. They will need to enable development of APIs and other extensions that allow them to embed solutions into various platforms and corporate systems. Orchestration is crucial, too. Banks must invest in capabilities that let them connect and automate corporate finance journeys—such as payment validation and scheduling— end-to-end. In addition, at the outset, cybersecurity and data privacy protections will need to be designed into the IT architecture in order to mitigate risks and enable the bank to respond efficiently to evolving compliance rules.

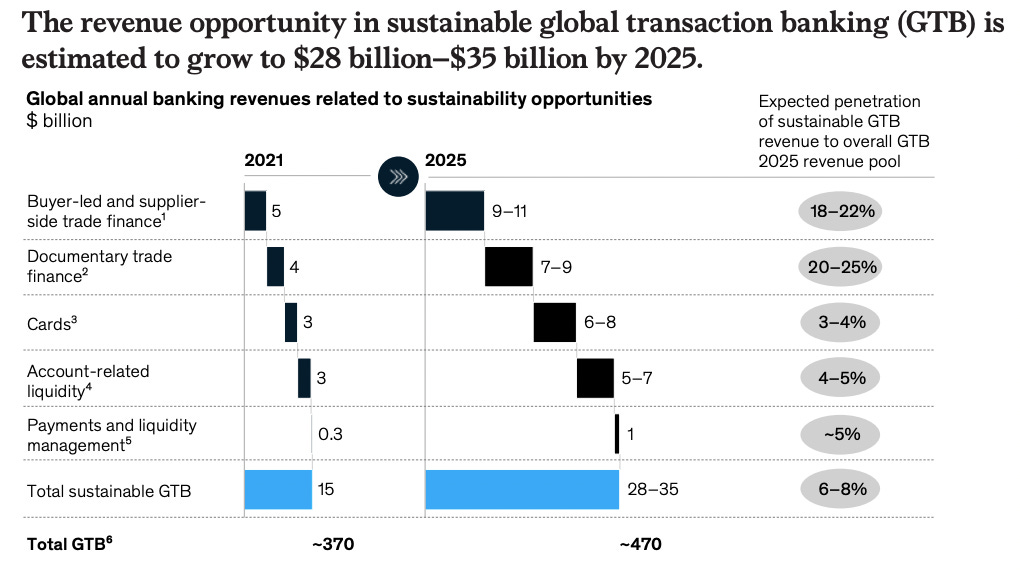

Sustainability in global transaction banking

Sustainable GTB products are cash management and trade finance products that support companies in their sustainability activities

We estimate that revenue from sustainable trade finance and cash management products will grow by 15 to 20 percent annually to total combined revenues of $28 billion to $35 billion in 2025,³ with market penetration reaching approximately 25 percent in trade finance products and 5 percent in cash management products

Banks’ current sustainability offerings are typically incorporated in traditional lending products, and growth in these products has been remarkably strong. According to Bloomberg estimates, the combined volumes of sustainability-rated debt instruments have grown approximately 80 percent per year, increasing from approximately $155 billion in 2017 to more than $1.6 trillion in 2021

embedding sustainability-tracking capabilities within core transaction banking services can be highly effective in improving companies’ performance on ESG metrics, as trade and payment transactions are systematic and recur frequently. What is more, trade finance rolls over frequently (every 30 to 90 days), which means that products such as supply chain finance (SCF), letters of credit, and guarantees have the potential to contribute disproportionately to new volumes in sustainable finance. The trade finance community—including financial institutions, export credit agencies, trade organisations, technology and service providers, and corporations—is focusing on various sustainability initiatives.⁶ Diverse banks offer sustainability-linked solutions, including deposit accounts backed by investments in sustainability rated assets and letters of credit issued for transactions in which the underlying asset (for example, batteries for electric vehicles) contributes to efforts to mitigate climate change. In addition, the number of requests for proposal (RFPs) for trade finance projects involving sustainability criteria is increasing, especially in the United States and Europe.⁷

Mckinsey payments report

Basic sustainable products

Documentary trade finance. For sustainable buyers or sustainability-linked transactions, banks could offer documentary trade finance, including letters of credit or guarantees, at better pricing and improved access. As an illustration, a letter of credit for the delivery of solar panels would qualify as a sustainable transaction, offered at a preferred rate to the buyer—and transferable as a sustainable trade asset.

Cards. On commercial cards, banks could offer favourable terms for purchase of sustainable goods or a mechanism to compensate for high emission expenses such as travel. In addition, this category could include other products such as acquiring and point-of-sale (POS) products with features such as rounding up each transaction to divert the surplus to sustainability projects or lowering POS or e-commerce fees for purchases of sustainable goods or purchases from merchants with higher sustainability scores.

Account-related liquidity. Banks could invest deposits in sustainable assets.

Payments and liquidity management. In payments, banks could offer favourable terms on transactions for sustainable underlying assets and with counter-parties scoring high on sustainability. In the area of liquidity management, banks could enable virtual accounts, which can be segregated from the account structure, to separate balances and transactions related exclusively to sustainable activities.

With so many untapped opportunities, what is holding back banks? We see three types of constraints limiting their ability to scale sustainable GTB products:

1. Lack of standards on several levels

Standards for sustainable digital trade documents.

Standard definitions of sustainable trade finance products

Standards for uniform sustainable trade finance data models.

Standards for sustainable trade finance APIs

2. Limited capital available for ecosystem development and operation

The capital available for investment is limited, which for banks and corporates alike poses a significant challenge to the implementation of a sustainable GTB offering. Further, a substantial investment is required to build the data platforms critical for the advanced sustainability products and services of the second and third waves

3. An economically challenging business model

Thank you for reading. Hope you enjoyed this post!

This is brilliant! Detailed yet distilled into small chunks to simplify the GP landscape.

Amazing analysis here.