Buy Now Pay Later - Primer

Buy Now Pay Later - Primer

Detailed walkthrough of the business model

Hey Everyone!

Over the past 3 months, I had the opportunity to intern with the leading BNPL player in Middle East (Tamara). This afforded me the chance to dive deep into the leading players across the globe and understand the nuances of how the major players run their operations.

With this post, my goal is to bring together my learnings and highlight the core elements of the industry. I try to tackle it by breaking the post into the following sections -

What is BNPL?

Different kinds of BNPL players

Key operating metrics and benefits of BNPL

Unit economics breakdown + operating expenses

Funding relationships and management

Ways to differentiate + building a competitive strategy

What is BNPL?

Buy Now Pay Later is a form of financing where customers have the opportunity to take their purchases but splitting the payments across numerous installments and over a period of time. The BNPL product as we see currently across the world has several key characteristics -

Omnichannel

Offering low or zero interest installment financing. This is usually in the form of Pay in 3, Pay in 4, Pay in 6 or Pay in 12 months.

BNPL players usually make money by charging merchants

Revenue from customers will only come in the form of late fees/ interest charged on late payments but is usually capped

Real time approval process

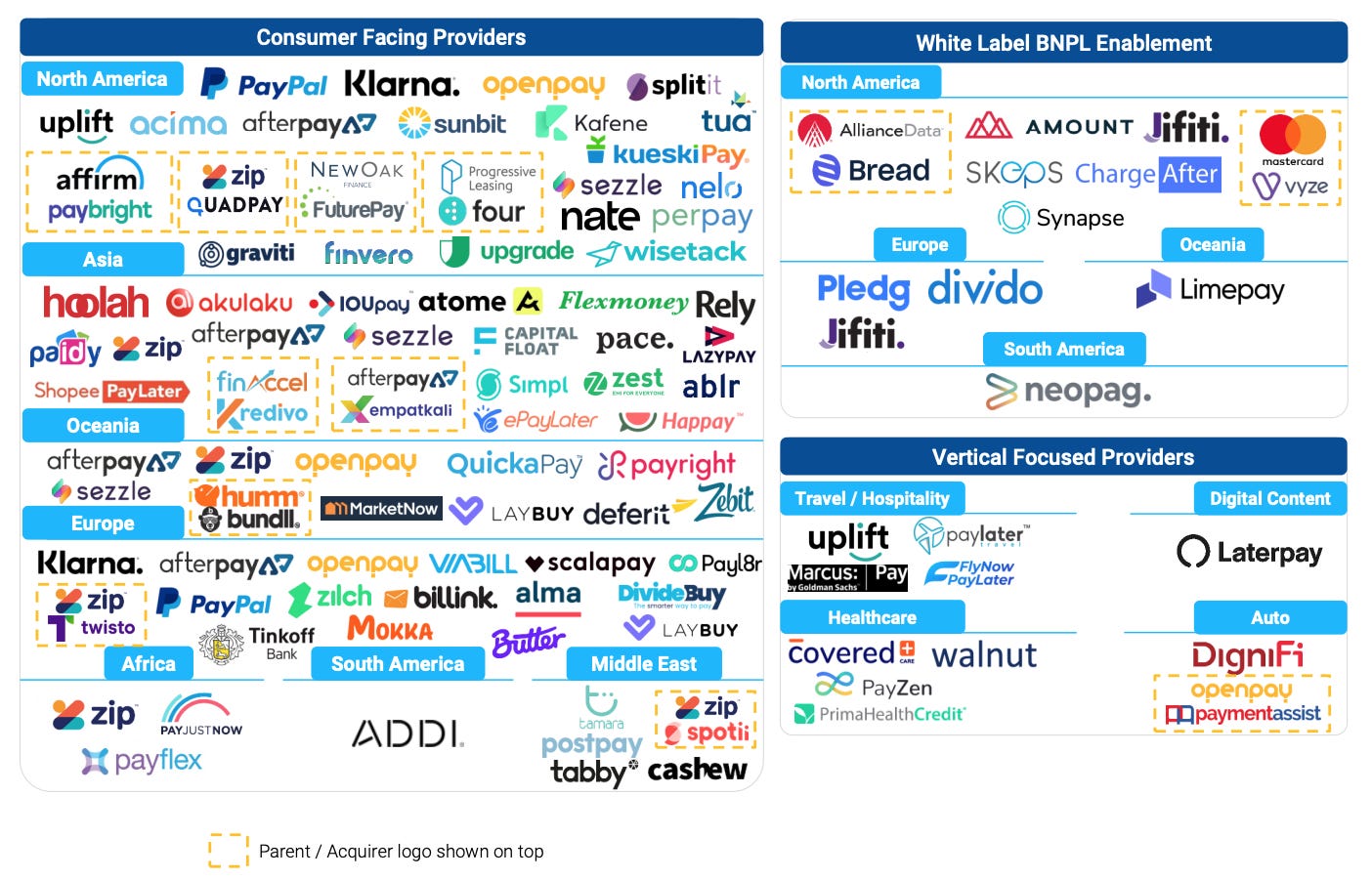

As seen below in the complete market mapping of BNPL players, the whole industry has become a force majeure especially as Covid-19 wrecked havoc on the global economy beginning March, 2020 and consumers primarily shifted to online shopping.

2020 saw the creation and entry of a lot of BNPL players across the globe. Klarna raised by and far the highest amount with close to $2.2 B in venture funding since beginning of 2020.

Different kinds of BNPL players

There are primarily 5 different types of GTM strategies that have been availed by companies -

Merchant facing model

This business model entails reaching out to merchants individually especially the larger ones and signing them on to the platform. BNPL players are known to either have a standard pricing or merchant by merchant pricing determined by various criteria’s that go into pricing decision. This could range from anywhere between 2 to 7 %.

In regards to smaller merchants, BNPL players provide the opportunity to follow a self serve model and integrate into the platform.

Consumer facing model

There are BNPL players that market directly to the consumer and issue actual/virtual cards to them. This allows them to bypass the need to acquire merchants and instead allows the consumer the ability to make a purchase at any merchant (contingent on a few criteria’s)

Integrations with Networks + PoS

Visa and MasterCard have come out with offerings that allow their partners to add the product as an offering of their own and hence provide customers installment payments.

Traditional banks

Legacy banks especially across Europe, Australia and U.S have started offering BNPL offerings to their consumers whether it is in-house development or white labels.

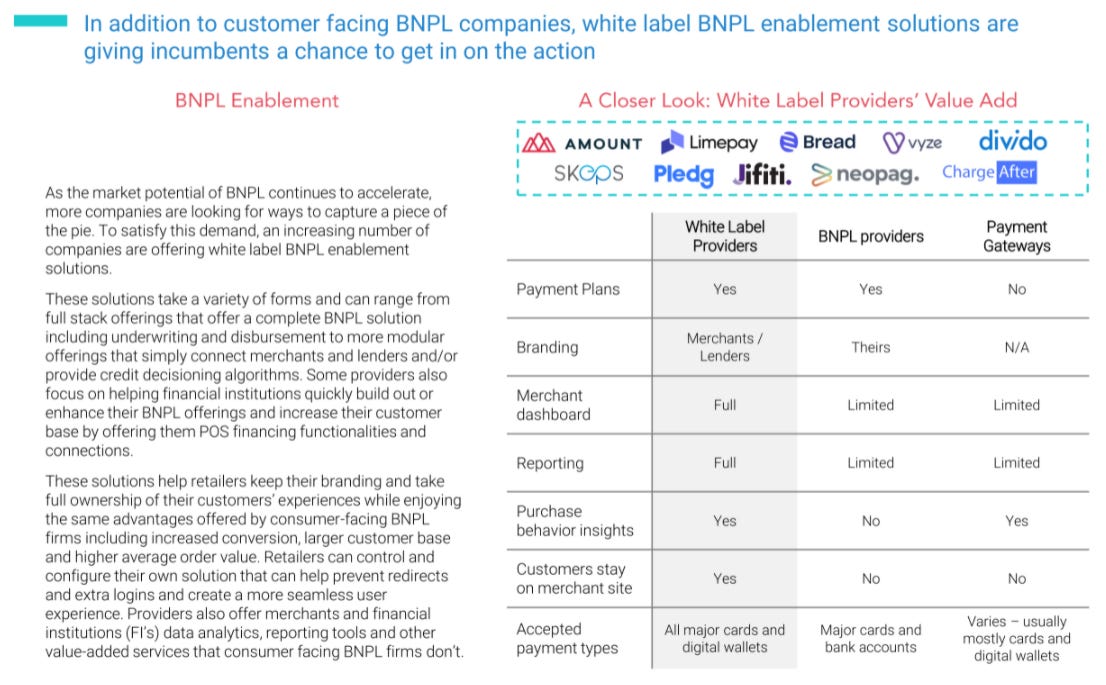

White label services

There are fintech players that have developed BNPL offerings allowing merchants and banks to integrate the product and offer it to their customers. With white-label services, the user of the service has the bonus of having their own branding, further developing the customer relationship, determining if the risk and lending needs to happen through its own balance sheet or through the provider of the white label BNPL service etc

Key operating metrics and benefits of BNPL

GMV (Gross Merchandise Volume) - Total value of all the transactions that have happened on the platform of the BNPL player.

Net captured amount - Total value of all the transactions that have been processed after refunds/cancellations

Active consumers

Monthly active customers

Yearly active customers

Transactions per customer

Number of merchants signed on to the BNPL platform

Net Transaction Margin (more on this below)

Ignoring certain specific issues that merchants face based on where they are located, existing solutions that merchants avail have shortcomings around the following areas:

Carts being abandoned/ difficult checkout process

Problems around engaging and converting customers

Addressing unaffordability

Lack of intelligence around customer data/ choices

Benefits around integrating and using a BNPL service - A core component of selling the BNPL product and convincing merchants revolves around the benefits that the product brings. These include but not limited to

Increased transaction size

Increased AOV(Average order value)

Increasing number of orders

Bring reluctant customers to market

Increasing customers and better conversion

Quick credit approval for customers

Increased repeat purchase rate

Better understanding of customer data and personalized marketing and promotional strategies

Unit economics breakdown + operating expenses

In having talked about the benefits, problem to be solved and issues currently being faced by merchants, I want to focus on the financial aspect of the business and the revenue and cost levers associated in running a BNPL player.

Product types

The most common type of product that is prevalent in the BNPL space seems to be the Pay in 4 product. What this usually entails is a down payment + 3 payments spread out across either 3 months or 3 payments across 6 weeks(2 week payment cycle).

Some of the other common products are -

Pay Later - No downpayment, one payment usually after a month.

Pay in 3

Pay in 6

Revenue components

Focusing specifically on the merchant facing model(described above under different kinds of players) as that is the most common route that BNPL players take, the revenue model has the following core components

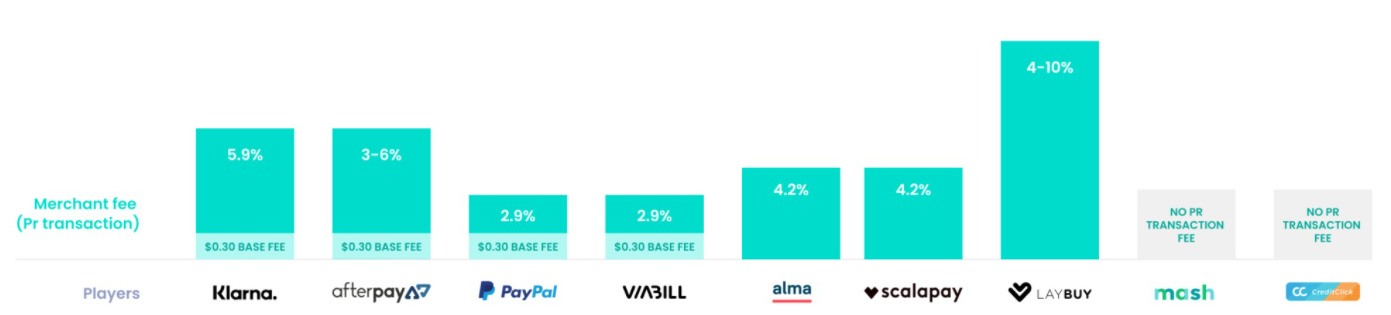

Earn fees from merchants - The other term for this is MDR(merchant discount rate).

Late fees - If the customer does not pay back in a timely manner, BNPL players will usually levy a one time late fee. See below for examples of what some firms charge.

Interest income on simple interest loans from consumers

Interchange income from cards issued to customers - For every transaction that a customer is engaging in through the card, the BNPL player depending on its arrangement with partner bank(in Klarna’s case, they have a banking license in certain geographical areas they operate in) will receive a cut of the interchange(usually a % of what the issuing bank gets to keep)

Gain(loss) on sales of loans - BNPL players like banks might not want to keep the loans on their balance sheet and could work with Investment Banks to securitize the loans and sell them. Similarly they have the option to buy back the loans from the partner banks that might be originating the lending and these transactions from an accounting perspective could have a profit/loss component to it.

Cost components

Provision for losses - For BNPL players especially across the new entrants, losses from customers not paying back usually is the largest component of your unit cost. Extreme focus and management of risks across merchants and customers can help create significant competitive advantages.

Usually, there is a step approach to how customers and credit limits work out. New customers will start off with a lower limit to manage risks and with regular payments, frequency of transactions and other criteria’s, they will see an increase in the limit. At the same time, if a customer was to miss a payment, they are prohibited from transacting again. This ban on making any other transactions is usually removed post the payment of any past dues.

Cost of debt - Almost all the BNPL players are not banks and have banking licenses thus taking away the opportunity to lend money based on the customer deposits. To meet this extensive funding need, BNPL players will either raise money through funding rounds, securitize loans, have access to lending warehouses with providers of capital etc.

Processing costs - When the transaction happens on a BNPL platform, the customer has to make the down payment depending on the option selected. Beyond that, they are also responsible for making monthly payments. These payments are usually made by customers through their debit or credit cards which incur a transaction fee/interchange. This fee is a cost that is usually borne by the BNPL player.

Recovery costs - When the customers do not pay in a timely manner, the clock on that debt being classified as bad debt starts. The BNPL players usually have the opportunity and will try to reach out to customers if they have dues pending and its within the 0-60 or 0-90 day timeframe. Beyond that usually firms will outsource the process to collection agencies to recover any amount that is outstanding. Hence, these costs fall under what we call as recovery costs.

Sales and marketing - Depending on the size and importance of a relationship with the merchant, BNPL players will sign on agreements with the merchants to engage in marketing and reach out to as many customers as possible.

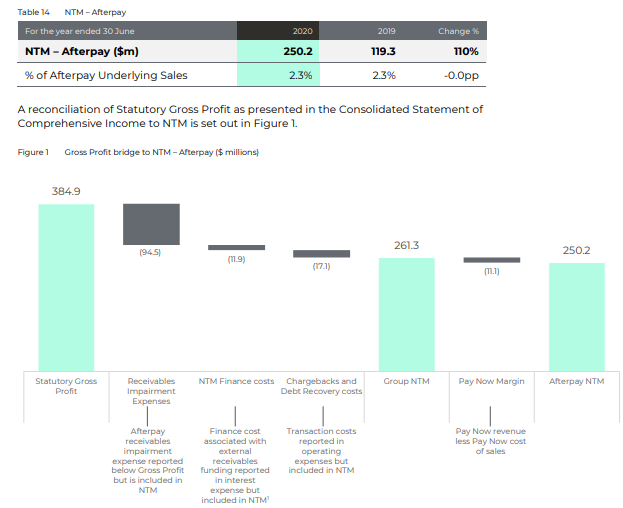

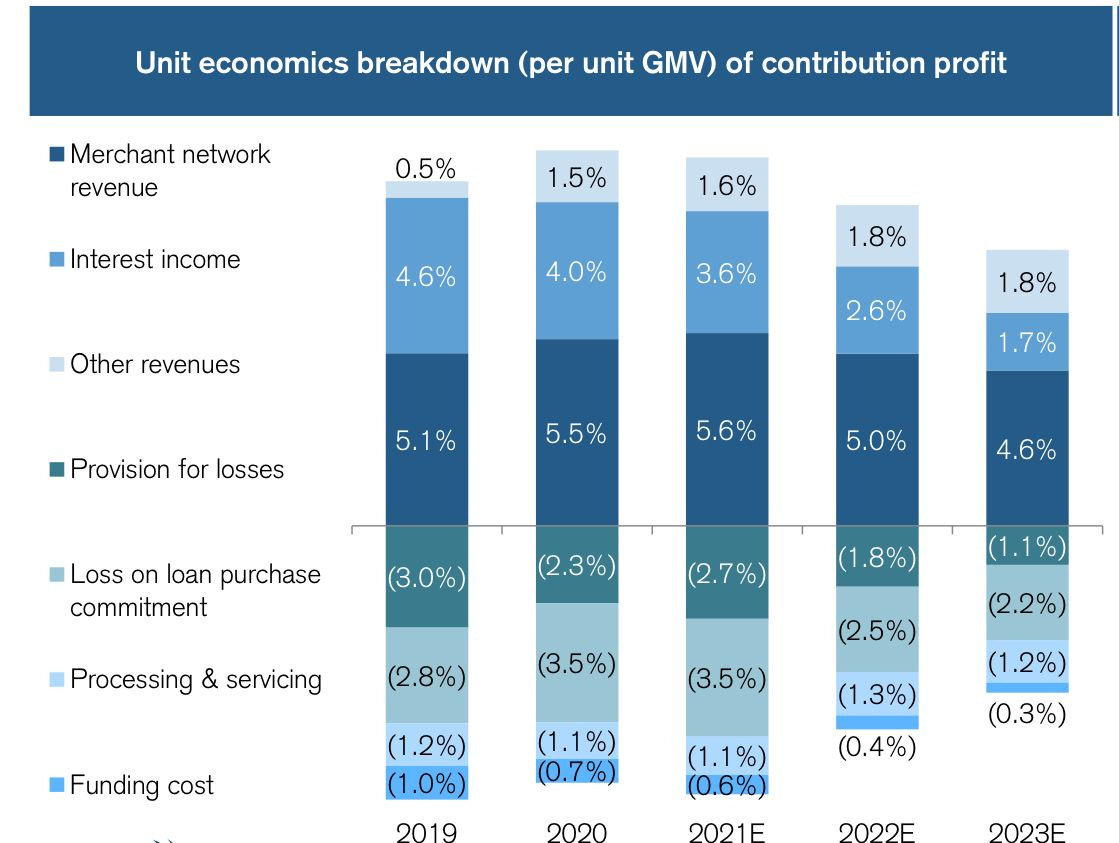

The culmination of all the above is what is called Net Transaction Margin. It is a non-GAAP/IFRS measure but is how the BNPL players are usually compared by. It is basically taking all the components that are part of the revenue and subtracting the costs directly associated with the purchase. Below is an example of how AfterPay reports its NTM.

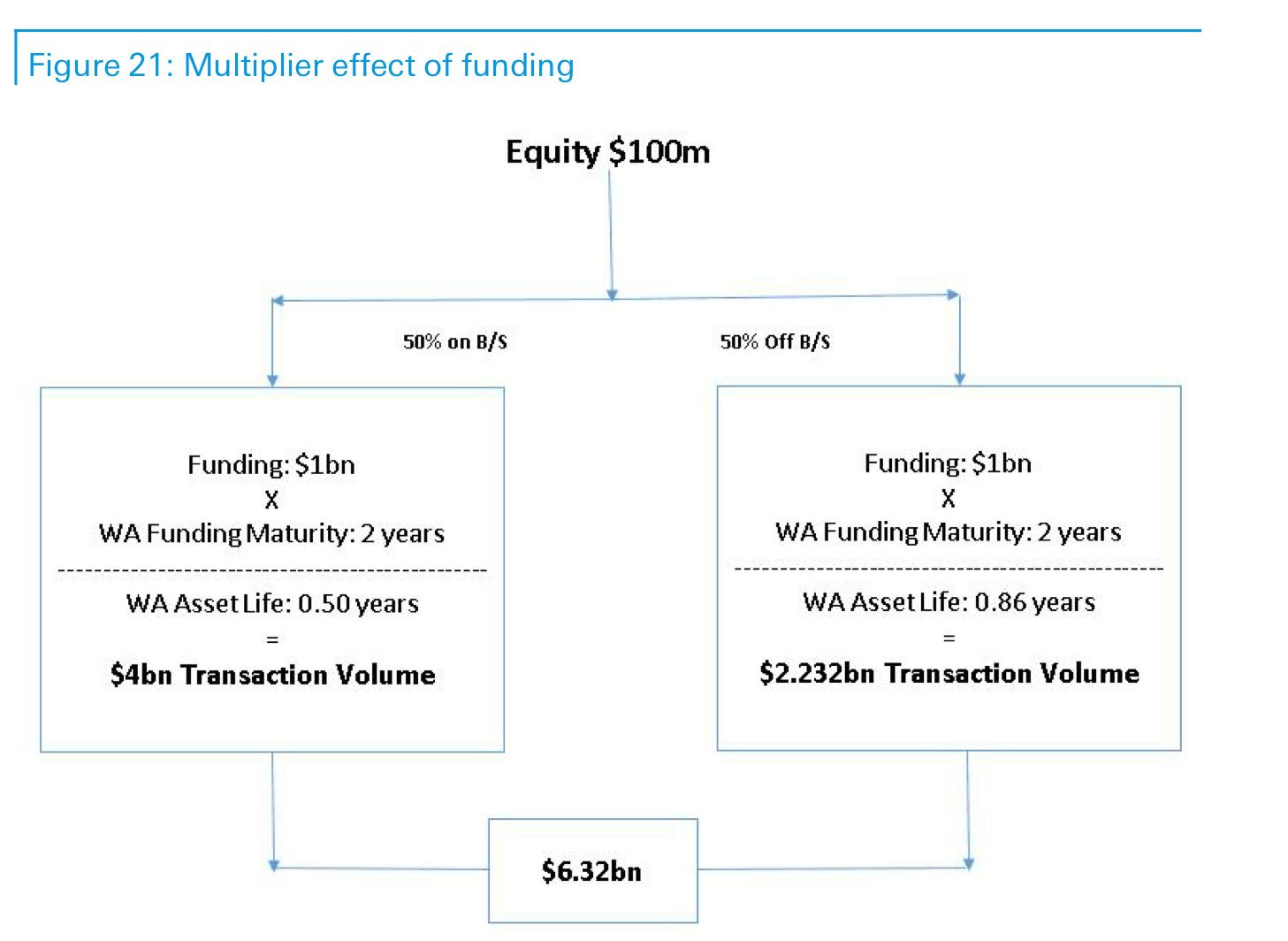

Funding relationships and management

As I highlighted in the cost components section about the cost of debt, depending on the arrangements and capital structure management, it can turn out to be one of the highest cost contributors in the income statement.

Its critical to understand that the with almost every other startup that is involved in raising funds from VCs/ Institutional investors, the cost of capital is usually high in the beginning given that the share of equity(in most circumstances has a higher cost of capital than all forms of debt) as a % of total capital is very high.

As the BNPL firms mature, what usually happens is what we see with some of the largest BNPL firms such as Klarna and Affirm. The access to different kinds of capital for when the company has matured is far more varied than the early stage capitals. These include but are not limited to

Equity

Debt

Warehouse facilities

Securitization of loans

Whole loan forward flow arrangement

Bank partnerships

The nature of this industry is such that lending is at the core of the operations. The differentiating factor is the short duration of the loans/assets and hence the asset-liability management which is at the core of banking operations is not something that is too big of a concern for the firms. Cash management is absolutely critical but as the loans are paid back beyond what is bad debt, it results in high velocity/turnover of the capital thus helping the BNPL firms earn a much higher return on top of its cost of capital which in itself trends lower as the firm matures.

Below is an example of the funding breakdown for AfterPay in their annual report that demonstrates how the combination of different sources comes together and allows them to engage in their lending operations.

Ways to differentiate + building a competitive strategy

There is no denying that over the past two years there have been numerous BNPL startups all vying for the market and believing in their ability to change the way consumers shop.

The two simplistic versions of what strategy is that I like is doing things that help you earn returns more than your cost of capital and what initiatives/decisions are you as a firm taking that your competitors are not. What I highlight below is by no means a comprehensive list but what I believe can really help differentiate the BNPL players and become a brand that is cherished and on the top of the consumers minds.

Omnichannel presence

Ability to build and enhance on merchant relationships

Creating a seamless experience for consumers across online and in-store experience

Loyalty programs

Co-marketing campaigns and providing value add to merchants and helping them differentiate within the app and across the web platform

Banking services - Enabling customers to have an end to end experience starting with bank accounts, credit/debit cards and integrating with a seamless shopping experience

Data and analytics around customer preferences, shopping experiences and bringing it all together to offer personalized recommendations

Extremely strong risk management practice. Going beyond the generic credit report and utilizing variate data elements to provide credit to customers from all walks of life

A lot of what BNPL firms have set out to accomplish also revolves around providing opportunities and lending to credit invisible people. This is only possible if the firms are able to build upon the plethora of data that they see on their customers and build proprietary models. This seeking out and providing value to customers that have been shunned by the banking industry and usually who have to resort to payday lending is an immense opportunity in itself and helps drastically skew the value proposition on the positive side.

Not forgetting that the reason customers especially young peoples preference for BNPL product is the ability to bring affordability to their purchases. This should be tied in together with understanding and ensuring proper financial health of the customers and ensuring that the firm engages in no predatory lending and recovery behavior for short term gains

Last but not the least - The network and flywheel effect. The image below from Affirm’s S-1 does a great job in describing the immense value a firm stands to gain if they get this right.

In bringing it all together, there are several reasons for my extreme bullishness in the growth story of the BNPL industry -

Possible permanence in the trend of ecommerce growth and share of retail transactions as seen in 2020-21

Growing share of Millennial and Gen X amongst shoppers and adaption of the payment method

Seamless experience for shoppers across online and offline channels

Adoption and launching of the BNPL product by traditional banks

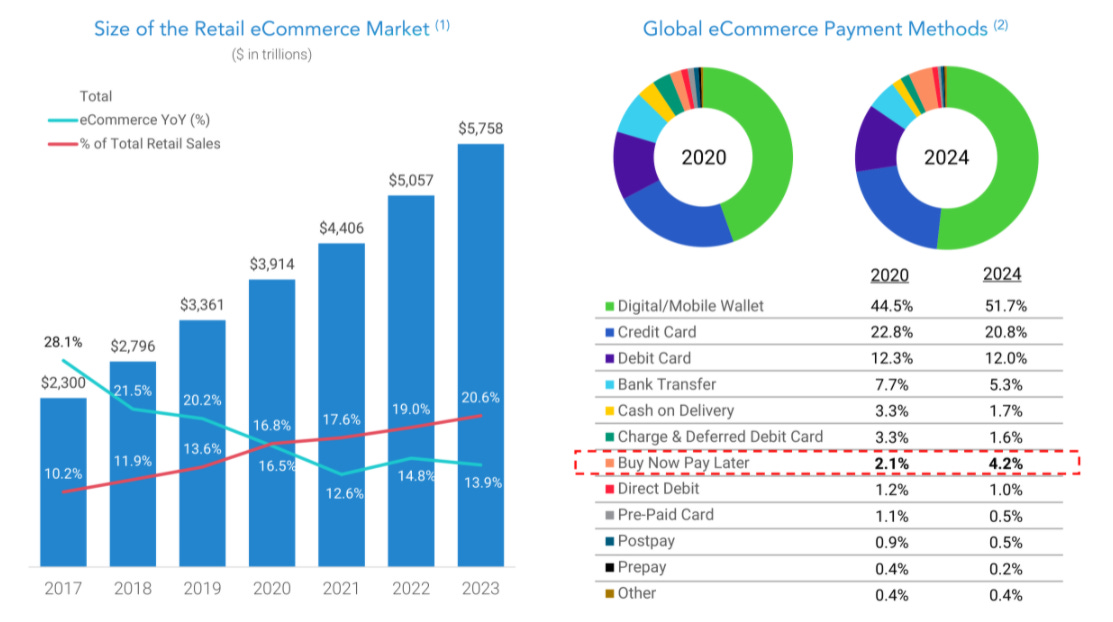

Despite the massive amount of fundraising amongst all the BNPL players, the industry is still in a nascent stage. The BNPL share across the global ecommerce market stood at a paltry 2.1%.

Resources

A deep-dive into Europe’s fast growing BNPL market

Jason Mikula - Buy Now Pay Later - Global Primer

Klarna annual report

AfterPay annual report

Affirm - S1

Barclays - Affirm research

Credit Suisse - Affirm research report